Active

There are no SAMM Changes as a result of this Policy Memo.

|

DEFENSE SECURITY COOPERATION AGENCY |

1/11/2011 |

MEMORANDUM FOR :

DEPUTY UNDER SECRETARY OF THE AIR FORCE FOR INTERNATIONAL AFFAIRS

DEPUTY ASSISTANT SECRETARY OF THE ARMY FOR DEFENSE EXPORTS AND COOPERATION

DEPUTY ASSISTANT SECRETARY OF THE NAVY FOR INTERNATIONAL PROGRAMS

DIRECTOR, DEFENSE CONTRACT MANAGEMENT AGENCY

DIRECTOR FOR SECURITY ASSISTANCE, DEFENSE FINANCE AND ACCOUNTING SERVICE - INDIANAPOLIS OPERATIQNS

DIRECTOR, DEFENSE INFORMATION SYSTEMS AGENCY

DIRECTOR, DEFENSE LOGISTICS AGENCY

DIRECTOR, DEFENSE LOGISTICS INFORMATION SERVICE

DIRECTOR, DEFENSE REUTILIZATION AND MARKETING SERVICE

DIRECTOR, DEFENSE THREAT REDUCTION AGENCY

DIRECTOR, NATIONAL GEOSPATIAL INTELLIGENCE AGENCY

DEPUTY DIRECTOR FOR INFORMATION ASSURANCE, NATIONAL SECURITY AGENCY

SUBJECT :

Execution and Closure Guidance for Pseudo Letters of Offer and Acceptance (Pseudo Cases) Financed with U.S. Appropriated Funds that have a Limited Period of Availability, DSCA Policy 11-06

The attached guidance provides clarification of execution and closure procedures for pseudo cases funded with U.S. appropriated funds that have a limited period of availability. Once funds expire for new obligation, specific attention must be provided to ensure all financial transactions are liquidated and cases closed before funds cancel.

None of the procedures in this'guidance are new; most can be found in DoD 7000.14-R, Department of Defense Financial Management Regulation. The procedures are simply presented in one document for ease of use in application to pseudo Letters of Offer and Acceptance/cases.

Should you have any questions concerning this guidance or require further clarification, please contact my action officer, Michele Kennedy, michele.kennedy@dsca.mil, 703-604-6578. For specific case information, please contact Matt Rothamel, matthew.rothamel@dsca.mil, 703-602-1321.

Ann Cataldo

Principal Director

Business Operations

ATTACHMENT :

As stated

CC :

STATE/PM-RSAT

DISAM

USASAC

SATFA

TRADOC

USACE

NAVICP

NETSAFA

AFSAC

AFSAT

AFCEE

JFCOM

SOCOM

EUCOM

CENTCOM

NORTHCOM

PACOM

AFRICOM

SOUTHCOM

TRANSCOM

Execution and Closure Guidance for

Pseudo Letters of Offer and Acceptance

(Pseudo Cases) Financed with

U.S. Appropriated Funds

that have a

Limited Period of Availability

Issued by DSCA-DBO

January 2011

Table of Contents

| Section | Page |

|---|---|

| REFERENCES | 1 |

| OVERVIEW | 1 |

| TIMELINE | 2 |

| DEFINITIONS | 3 |

| RECOMMENDATIONS | 3 |

| REQUIREMENTS | 5 |

| Expiring Funds | 5 |

| Canceling Funds | 8 |

| Post Cancellation Payments | 9 |

| SUMMARY | 11 |

| ATTACHMENTS | 11 |

Execution and Closure Guidance for

Pseudo Letters of Offer and Acceptance (Pseudo Cases)

Financed with U.S. Appropriated Funds that have a

Limited Period of Availability

This document consolidates and clarifies the application of existing financial and fiscal guidance to pseudo cases funded with United States Government (USG) appropriations that have a limited period of availability. The Department of Defense Financial Management Regulation (DoD FMR), DoD 7000.14-R, contains explicit guidance concerning expiring and canceling funds. A listing of volumes and chapters addressing this policy are at Attachment A. Refer also to the Federal Acquisition Regulation (FAR) and Defense Federal Acquisition Regulation (DFAR). Specific references within this guidance are also highlighted at Attachment A.

Foreign Military Sales (FMS) Trust Fund budget authority is classified as permanent, indefinite, no-year authority. Budget authority associated with FMS cases is treated as non-expiring money. Many of the pseudo cases implemented via the FMS Trust Fund, however, are financed with expiring appropriations and these funds are required to be obligated in the FMS Trust Fund prior to the appropriation expiring, and expended prior to the appropriation canceling. This guidance does not address pseudo cases that implement requirements and funding transferred to DSCA under authority of section 632(b) of the Foreign Assistance Act of 1961, as amended. DSCA Programs (PGM) normally controls processes associated with such transfers.

All financial and acquisition documents include a fund cite that reflects the appropriation and year of expiration. The appropriation fund cite financing pseudo cases reflects an expiration date; however, once the funds are transferred into the FMS Trust Fund, the FMS Trust Fund fund cite is used on financial documents. Therefore, do not rely on the fund cite associated with the case to determine whether funds should be treated as expiring/canceling. The first indicator that a case is not a traditional FMS case is that within the line of accounting, the FMS country code is depicted by an alpha-numeric designator versus an alpha-alpha designator. This unique country code is assigned for each specific authority (see Attachment B). [Note: Some NATO organizations' FMS country codes also have alpha-numeric designators. Refer to the SAMM, Table C4.T2. for a complete listing of FMS country codes.]

When the pseudo cases are financed with funds that are required to be treated as expiring/ canceling, the funds in the FMS Trust Fund must be obligated within the period of appropriation availability, expended within five years after the appropriation expires for new obligations, and any unexpended funding returned to the U.S. Treasury or the original funds holder before the end of the fifth year after funds expire for obligation. Accordingly, pseudo cases and contracts associated with those cases must be final closed prior to returning the unexpended funds. Guidance unique to a specific program may be provided under separate cover.

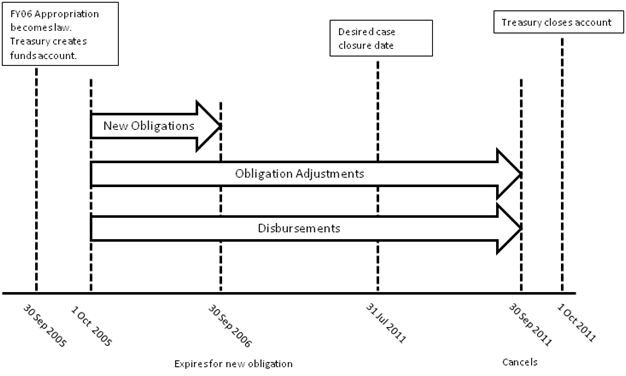

The following graphic depicts the typical timeline for an annual (1-year) authorization/ appropriation. Many pseudo cases are funded with annual (1-year) appropriations, such as the section 1206 program funded with Defense-wide Operation and Maintenance (O&M). The Afghanistan Security Forces Fund (ASFF) and Iraqi Security Forces Fund (ISFF) have either a 1-year or 2-year period of availability, depending on the authorization. The Pakistan Counterinsurgency Fund (PCF) has a two-year period of availability and the Pakistan Counterinsurgency Capability Fund (PCCF), when merged with PCF, has a three-year period of availability. Care must be taken to understand the nature of the appropriation underlying a pseudo case. [Attachment B further reflects the year of authorization/appropriation, when the funds expire, and when the funds cancel.]

In the example below, the appropriation is for one year beginning 1 Oct 2005 (FY 06), expiring 30 Sep 2006, and canceling 30 Sep 2011. Barring any specific legislative language, the appropriation cancels five years after the funds expire for obligation.

To ensure a pseudo case is closed in sufficient time to allow funds to be returned to the U.S. Treasury by 30 September of the year of cancellation, all open funding lines against such documents should be closed by 31 July of the year of cancellation. This would mean that the Contracting Officer's Representative (COR), or government representative, will ensure that vendors have submitted all invoices and they have been paid in full. In addition, the pseudo cases must be reconciled and final closed.

To ensure this guidance is interpreted consistently, the following definitions from the DoD FMR Glossary are provided for reference:

-

Annual (1-Year) Authority. Annual budget authority is available for obligation only during a specified fiscal year and expires at the end of that time.

-

Period of Availability. The period of time in which budget authority is available for original obligation.

-

Expired Account or Appropriation. Appropriation or fund account in which the balances no longer are available for incurring new obligations because the time period available for incurring such obligations has ended. However, the account remains available for 5 years to process disbursements, collections, and within scope adjustments of original obligations.

-

Adjustments to Expired or Canceled Accounts. Increases or decreases to obligations or expenditures. Adjustments involve recording obligations or expenditures that were made or incurred, but not recorded, during the period prior to expiration or cancellation of the account.

-

Closed/Canceled Accounts. An appropriation that has been closed in accordance with 31 U.S.C. 1551-1557. It also includes an appropriation that otherwise would have been closed by 31 U.S.C. 1551-1557, but has not been closed by the Department of the Treasury because the appropriation has a negative balance. When balances are canceled, the amounts are not available for obligation or expenditure for any purpose.

Pseudo cases should contain a standard note, "Funds Expiration, Purpose, and Availability," that defines the source of the appropriation and the period of availability.

There are several actions that may assist the Implementing Agency and the case manager in assuring the case closure timeline is met:

-

Review the pseudo case to understand the nature of the appropriation.

-

Involve the contracting community up-front and early.

-

Firm fixed-price contracts/line items, when possible, should allow for a less complex contract close-out. (See FAR 4.804-1)

-

Include finance instructions in Section G (or equivalent of the Request for Proposal (RFP)) of the contract to ensure all are aware of the expiring/ canceling nature of the funds being applied. An example follows:

This contract action contains funds that expire for obligation on 30 Sep 20XX. These funds cancel 30 Sep 20(XX+5) and will not be available for any funding adjustments after that date. All contract actions and final billings must be complete in sufficient time for cases to close by 31 Jul 20(XX+5).

This same language should be used on any other funding document to ensure the executor of the document is aware of the expiring/canceling nature of the funding.

-

The contract can specify a method of submitting payment requests (see e.g., DFARS 252.232-7003, "Electronic Submission of Payment Requests and Receiving Reports").

-

-

The customer point of contact or designated COR shall maintain oversight of deliverables and ensure inspection/acceptance, and timely processing of proper contractor invoices (see FAR 32.905).

-

Review and reconcile documentation more frequently; this results in less fewer mistakes and less correction action. The DoD FMR, Volume 3, Chapter 8, Standards for Recording and Reviewing Commitments and Obligations, requires a Triannual Review of commitments, obligations, accounts payable, and accounts receivable. It further states:

-

The goal in performing the Triannual Review is to increase DoD Component's ability to use available appropriations before they expire and ensure remaining open obligations are valid and liquidated before the cancellation of the appropriation. The Triannual Reviews should be particularly rigorous in reviewing commitments and obligations of appropriations prior to their expiration. Attaining the Triannual Review goal is contingent on effective integration and synchronization of the Funds Holder (Resource Manager), Accounting, Program Management, Contracting Officers, and Acquisition/ Logistics functions during each Triannual Review process. The responsibility for successfully completing the Triannual Review is a collaborative effort. The integrating of all the stakeholders into the review process will allow for an effective review of commitments, obligations, contracts, and all fiscally related requirements.

-

-

Communicate at all levels to ensure the participants in the acquisition process are aware of the current status and what needs to occur to ensure closure occurs as required.

-

If required, ensure the additional workload of managing and closing cases funded with expiring funds is factored into development of annual FMS Administrative Surcharge budget submissions.

Managing expiring funds associated with pseudo cases implemented in the FMS Trust Fund is a challenge. Realizing the inherent limitations of managing expiring funds in the FMS system and following these guidelines can improve program execution. With adequate planning and timely execution, participants can work together to overcome potential obstacles.

[Note: Dates are notional. Refer to the annual DSCA Standard Operating

Procedures (SOP) for Train and Equip Programs for specific dates.]

-

Residuals: The FMS process requires the Implementing Agencies to implement a pseudo case in the FMS Trust Fund, which creates the obligation authority to fund the execution of the case. Often, the estimated value of the implemented case is greater than the actual obligation authority needed to execute the case. Excess obligation authority on these implemented pseudo cases is referred to as residual funds (not to be confused with residual value, which relates to capital asset valuation). The use and return of residual funds can be a significant challenge due to the short time remaining for obligation after the funds have been identified. Therefore, Implementing Agencies should be reviewing their cases/lines for possible residual funding throughout the period of availability of the funds to ensure the funds can be executed prior to expiration. Implementing Agencies should also consider Contract Audit Services (CAS) and Small Case Management Line (SCML) values in determining the actual amount of residual funds available. Options for use of residual funds, in priority order, follow:

-

Use funds for other requirements within the existing pseudo case, assuming that the change is consistent with any departmental or congressional authorization or program notification.

-

If the funding authority for the pseudo case allows, move the residual funds to another pseudo case financed under the same authority.

-

Deobligate funds and reduce case value by providing a case amendment or modification. DSCA will then direct DFAS to take appropriate action to return residual funds to the appropriate account.

-

-

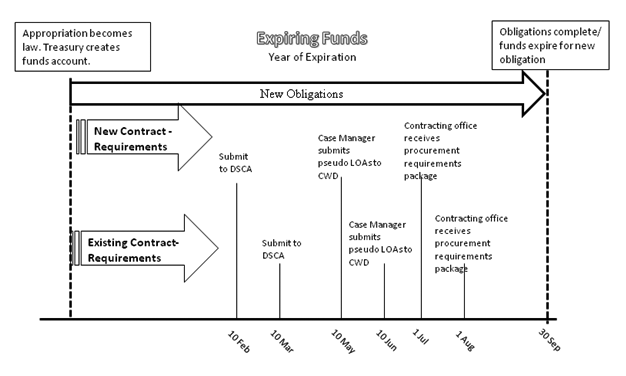

Deadlines. To ensure funds are obligated prior to their expiration (30 Sep of the applicable fiscal year), DSCA has developed the following timelines for use by the geographic Combatant Commands and the Implementing Agencies: [Note: While the dates will change with the issuance of the annual DSCA SOP for the Train and Equip Programs, the following dates are provided for illustrative purposes and are in line with past dates issued in the SOP. Please refer to the SOP for the specific dates.]

-

On/About 10 February - Submit New Contract Requirements to DSCA. This deadline is for new contract requirements to be submitted to DSCA (PGM for 1206 and OPS for all others). This affords the necessary time for DSCA (OPS and PGM) to task the Implementing Agency and to give the Implementing Agency the opportunity to write the corresponding pseudo LOA documents. The activity developing the requirement is responsible for submitting sufficient detail to order the proper item from the supply system or purchase it through the acquisition process. The risk of failure increases if the requirements for these cases are not sent to the Implementing Agency by the deadline. Complex new contracts/high dollar value cases will require the longest time to process and should be considered early when identifying requirements.

-

On/About 10 March - Submit Requirements that can use Existing Contracts to DSCA. This deadline is for new requirements to be submitted to DSCA (OPS and PGM as applicable) for defense items/services that can be supported with existing contracts and the Implementing Agencies are then able to write the pseudo LOA documents. Some existing contracts will allow identification of requirements after this deadline; however, requirements should be simple and easily met. The length of time to develop and implement a pseudo case and subsequently obligate funds on an existing contract vehicle ultimately depends on the complexity of the requirement. [NOTE: The current practice of using tranche notifications for Section 1206 cases may make meeting these dates for final tranche notifications very difficult. Such short-fuse cases will be treated on an exception basis.]

-

On/About 10 May - Submit All New Requirements to the DSCA Case Writing Division (CWD). This deadline allows the case manager to complete and submit to DSCA CWD all pseudo LOAs that require contracting of items not currently supported by an existing contract vehicle. Initial procurement actions may require the acquisition community to take more extensive contractual actions in order to complete the contracting action, get the item on contract, and identify residual excess funding. This deadline allows DSCA, the Defense Finance and Accounting Service (DFAS), the Department of State, the Office of the Secretary of Defense (OSD) and the Implementing Agency adequate processing time to ensure contracting actions are provided to the contracting elements by 30 June. This also allows the contracting officer three months to execute a binding contract, order, or other similar agreement and to record the associated obligation and to identify and reuse residuals.

-

On/About 10 June - Submit All Requirements that can use Existing Contracts to the DSCA CWD. This deadline is for the Implementing Agency case manager to complete and submit to DSCA CWD, all pseudo LOAs requiring contracting of items or services currently supported by an existing contract vehicle. This deadline also applies to Defense Working Capital Fund (DWCF) items or any off-the-shelf requisition items. This allows DSCA, DFAS, the Department of State, and OSD sufficient processing time to ensure contracting action delivery to Implementing Agency contracting elements by 1 August. Once received, the Implementing Agency will have until 30 September (two months) to establish the obligation and to identify and reuse residuals.

-

On/About 1 July - Submit All Procurement Requirements for Award of New Contracts to the Contracting Office. The procurement requirements package should be provided to the contracting office for pseudo cases requiring the award of a new contract.

-

On/About 1 August - Submit All Procurement Requirements that Can Use Existing Contracts to the Contracting Office. The procurement requirements package should be provided to contracting office for pseudo cases requiring amendments to existing contracts.

-

No Later than 30 September - Award and Obligate All Contract Actions. All contract actions are awarded and funds obligated.

-

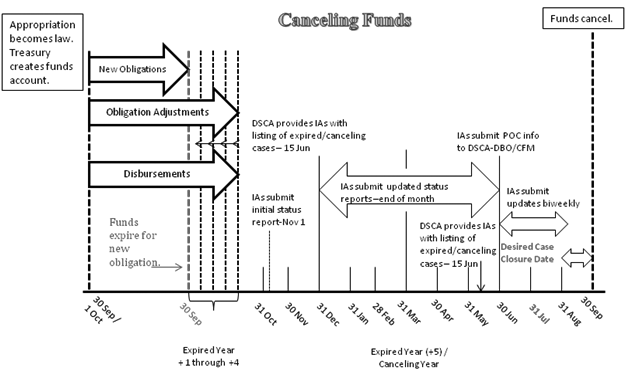

By 15 June of each year, DSCA Business Operations, Country Financial Management Division (DBO/CFM) will provide the Implementing Agencies with a listing of specific case designators for cases that have expired funds subject to cancelation that must be closed prior to the end of the subsequent fiscal year (year 5 after funds expire). The Implementing Agencies will be reminded that obligations must be liquidated to ensure case closure by 31 July of the canceling fiscal year and that funding will not be available for any billings/expenditures after 30 September of that year due to cancelation of the funds. [Note: By 15 November of each year, DSCA DBO/CFM will provide a listing of all cases for which funds have expired for new obligation, but have not yet canceled. This will be an update of the 15 June listing plus any other open cases - i.e., if 2011 is the canceling year, the listing would also include cases that cancel in 2012, 2013, 2014, 2015, and 2016.]

The case is then a candidate for closure when (1) all ordered items have been physically delivered, (2) all ordered services performed (i.e., supply/services complete), and (3) the period of funds availability for new obligation has expired, in addition to all other conditions of the pseudo case having been fulfilled.

DFAS Indianapolis shall review the closure certificate and perform actions to close the pseudo LOA document in the Defense Integrated Finance System (DIFS). If DFAS Indianapolis has questions on the closure certificate, they shall contact the Implementing Agency listed on the certificate. Implementing Agencies shall check the DIFS closure inventory on an as needed basis to determine which pseudo cases have been closed. DFAS Indianapolis should close pseudo cases containing no inhibitors within 30 days of closure certificate and "C1" closure transaction receipt.

The format at Attachment C is to be used to provide periodic updates on the status of canceling fund pseudo cases during the year of funds cancelation. With this update, the Implementing Agency should also provide any cases with known inhibitors that will not allow case closure. This form shall be provided to DSCA DBO/CFM as indicated below, or as otherwise directed:

| Update | Timeframe |

|---|---|

| Initial Submission: | 1 November |

| Monthly Submissions: | End of month from December - June |

| Bi-Weekly Submissions: | End of week July-August |

| Weekly Submissions: | End of week during September |

By 30 June of the fiscal year preceding funds cancelation, the Implementing Agencies shall provide contact information to the DSCA DBO/CFM expiring funds focal point as to who will serve as the single point of contact/facilitator within the Implementing Agency. This contact shall establish periodic teleconferences with stakeholders and with DSCA DBO/CFM to review all canceling pseudo cases and, most importantly, any case at risk of not closing by 31 July. Further, this individual shall prepare the "due outs" and manage follow-up action(s) for their Implementing Agency. The established telecons will afford the opportunity to understand the details of any pseudo case issue(s) and avoid possible misinterpretation/misstatement as they are staffed through the chain of command and at DSCA. The Implementing Agency contact shall be proactive and lead the stakeholders within their respective Implementing Agency to timely pseudo case closure.

Before an appropriation cancels, the Implementing Agency must identify, to DSCA, valid unliquidated obligations subject to closure to determine whether appropriations are available for future adjustments or payments against such obligations. Also the Implementing Agency must confirm whether adequate resources are available to pay for obligations that will cancel within an account (DoD FMR, Volume 3, Chapter 10, 100201.D.) If funds are required for pseudo cases where funds have expired/canceled, DSCA must be contacted for approval. Refer to DSCA Policy 10-08, dated January 29, 2010, subject: "DoD Appropriated Funds Prior Year Activity."

Per the DoD FMR, Volume 3, Chapter 10, 100201.F, when a currently available appropriation is used to pay an obligation, which otherwise would have been properly chargeable (both as to purpose and amount) to a canceled appropriation, the total of all such payments from that current appropriation may not exceed the lesser of:

- The unexpended balance of the closed/canceled appropriation (the unexpended balance is the sum of the unobligated balance plus the unpaid obligations of an appropriation at the time of closure/cancellation, adjusted for obligations and payments which are incurred or made subsequent to closure/cancellation, and which would otherwise have been properly charged to the appropriation except for the closure/cancellation of the appropriation);

Example:Fiscal Year FY 2005 O&M Appropriation = $1.000B Obligations = $0.950B Unobligated = $0.050B Unpaid Obligations = $0.150B Adjustments = ($0.025B) Unexpended Balance = $0.175B

OR - The unexpired unobligated balance of the currently available appropriation;

Example:Fiscal Year FY 2011 O&M Appropriation = $1.500B Obligated = $0.750B Unexpired/Unobligated = $0.750B

OR - One percent of the total original amount appropriated to the current appropriation being charged.

Example:Fiscal Year FY 2011 O&M Appropriation = $1.500B 1% = $0.150B -

For annual accounts, the 1 percent limitation is of the annual appropriation for the applicable account--not total budgetary resources (e.g., reimbursable authority).

-

For multiyear accounts, the 1 percent limitation applies to the total amount of the appropriation. As an example, if a multiyear account enacted for fiscal year 2007 through fiscal year 2008 was $100 million, then the 1 percent limitation in fiscal year 2007 would be $1 million. At the end of fiscal year 2007, if $650,000 had been used for payment of obligations of closed/canceled accounts, then the amount available to be used for such payments in fiscal year 2008 would be $350,000 ($1,000,000 minus $650,000).

-

For contract changes [under which a contractor is required to perform additional work], charges made to currently available appropriations shall have no impact on the 1 percent limitation rule. That is, the 1 percent (of the currently available appropriation) amount shall not be decreased by the charges made to current appropriations for contract changes.

-

None of the procedures documented herein are new. Attention paid early and throughout the life of a pseudo case to ensure deliveries, final billings, and reconciliation of all financial records occur in sufficient time to close the case in the year of funds cancellation, if not before, will maximize the ability to accomplish the mission, fully fund requirements, and minimize the risk of unexpended funds. For a ready reference, a notional timeline of actions is provided at Attachment D.

- Attachment A - References

- Attachment B - Pseudo Country Codes

- Attachment C - Canceling Funds Report Example

- Attachment D - Notional Timeline

Department of Defense (DoD) Financial Management Regulation (FMR) References:

| Volume | Chapter | Title |

|---|---|---|

| 3 | 8 | Standards for Recording and Reviewing Commitments and Obligations |

| 3 | 10 | Accounting Requirements for Expired and Closed Accounts |

| 3 | 13 | Receipt and Distribution of Budgetary Resources Departmental Level |

| 3 | 15 | Receipt and Use of Budgetary Resources Execution Level |

| 4 | 3 | Receivables |

| 6A | 4 | Appropriation and Fund Status Reports |

| 6B | 4 | Balance Sheet |

| 6B | 4 | Statement of Budgetary Resources |

| 10 | 7 | Prompt Payment Act |

| 10 | 12 | Miscellaneous Payments |

| 10 | 18 | Contractor Debt Collection |

| 14 | 2 | Antideficiency Act Violations |

Federal Acquisition Regulation (FAR) References:

- FAR - http://farsite.hill.af.mil/

- FAR 32.905 - http://farsite.hill.af.mil/otcgi/llscgi60.exe?ACTION=Highlight&QUERY=%33%32%2E%39%30%35&OP=and&DB=2&SORTBY=%54%49%54%4C%45&SUBSET=SUBSET&FROM=1&SIZE=50&ITEM=2#P1288_200680

Defense Federal Acquisition Regulation (DFAR) References:

- DFAR - http://www.acq.osd.mil/dpap/dars/dfarspgi/current/index.html

- DFAR 252.232-7003 - http://www.acq.osd.mil/dpap/dars/dfars/pdf/r20100713/252232.pdf

ATTACHMENT B - PSEUDO COUNTRY CODES

Part I: Department of Defense Appropriations and Related Authorities

| Program | Pseudo Code | Authority Fiscal Year | Expiring Fiscal Year | Canceling Fiscal Year | Public Law |

|---|---|---|---|---|---|

| Train and Equip Authority for the Afghanistan National Army | Y2 | FY04 | FY04 | FY09 | See 1107 of FY 04 Supplemental |

| Train and Equip Authority for the New Iraqi Army | Y3 | FY04 | FY04 | FY09 | See 1107 of FY 04 Supplemental |

| Section 9006 of FY05 Defense Appropriations Act for Afghanistan | Y5 | FY05 | FY05 | FY10 | P.L. 108-287 |

| Section 9006 of FY05 Defense Appropriations Act for Iraq | Y6 | FY05 | FY05 | FY10 | P.L. 108-287 |

| National Defense Authorization Act (Section 1206) | B4 | FY06 | FY06 | FY11 | P.L. 109-163, Sec. 1206 |

| Emergency Supplemental Appropriations Act for Defense and for the Reconstruction of Iraq | Y7 | FY04 | FY06 | FY11 | P.L. 108-106 |

| Afghanistan Security Forces Fund - Emergency Supplemental Appropriations Act | Y8 | FY05 | FY06 | FY11 | P.L. 109-13 |

| Iraq Security Forces Fund - Emergency Supplemental Appropriations Act | Y9 | FY05 | FY06 | FY11 | P.L. 109-13 |

| Emergency Supplemental Appropriations for Afghanistan Security Forces Fund | B2 | FY06 | FY07 | FY12 | P.L. 109-234 |

| Emergency Supplemental Appropriations for Iraq Security Forces Fund | B3 | FY06 | FY07 | FY12 | P.L. 109-234 |

| National Defense Authorization Act (Section 1206) | B5 | FY07 | FY07 | FY12 | P.L. 109-364, Sec. 1206 |

| Fiscal Year 2007 DoD Appropriations Act for Afghanistan Security Forces | B6 | FY07 | FY08 | FY13 | P.L. 109-289, supplemented by P.L. 110-28 |

| Fiscal Year 2007 DoD Appropriations Act for Iraq Security Forces Fund | B7 | FY07 | FY08 | FY13 | P.L. 109-289, supplemented by P.L. 110-28 |

| National Defense Authorization Act (Section 1206) | B8 | FY08 | FY08 | FY13 | P.L. 109-364 |

| National Defense Authorization Act (Section 1206) | B9 | FY09 | FY09 | FY14 | P.L. 110-417 |

| Consolidated Appropriations Act, Afghanistan Security Forces Fund | E3 | FY08 | FY09 | FY14 | P.L. 110-161 |

| Consolidated Appropriations Act, Iraq Security Forces Fund | E4 | FY08 | FY09 | FY14 | P.L. 110-161 |

| Supplemental Appropriations Act, Afghanistan Security Forces Fund | E5 | FY09 | FY09 | FY14 | P.L. 110-252 |

| Supplement Appropriations Act, Afghanistan Security Forces Fund | E6 | FY09 | FY10 | FY15 | P.L. 110-252 |

| Supplemental Appropriations Act, Pakistan Counterinsurgency Fund | G2 | FY09 | FY10 | FY15 | P.L. 111-32 |

| Supplemental Appropriations Act, Iraq Security Forces Fund | G3 | FY09 | FY10 | FY15 | P.L. 111-32 |

| National Defense Authorization Act and Department of Defense Appropriations Act (Section 1206) | G7 | FY10 | FY10 | FY15 | P.L. 111-84 and P.L. 111-118 |

| Supplemental Appropriations Act, Pakistan Counterinsurgency Capability Fund as transferred into Pakistan Counterinsurgency Fund | G4 | FY09 | FY11 | FY16 | P.L. 111-32 |

| National Defense Authorization Act for FY 2010 (P.L. 111-84) and Department of Defense Appropriations Act, 2010 (P.L. 111-118), as supplemented by P.L. 111-212 Afghanistan Security Forces Fund | G5 | FY10 | FY11 | FY16 | P.L. 111-84, P.L. 111-118, and P.L. 111-212 |

| Supplemental Appropriations Act, 2010 (P.L. 111-212) Iraq Security Forces Fund | G8 | FY10 | FY11 | FY16 | P.L. 111-212 |

| DoD Counternarcotics Program, Section 1033 | S7 | N/A | Var | Var | NDAA, Sec. 1033 |

| DoD Counternarcotics Program, Section 1004 | S8 | N/A | Var | Var | NDAA, Sec. 1004 |

| Presidential Drawdowns for Afghanistan | S9 | N/A | Var | Var | FAA, Sec. 506(a)(1) |

Part II: Department of State Related Authorities

| Program | Pseudo Code | Authority Fiscal Year | Expiring Fiscal Year | Canceling Fiscal Year | Public Law |

|---|---|---|---|---|---|

| FAA, Section 632(b) | S4 | N/A | Var | Var | FAA, Sec. 632(b) |

* Refer to the SAMM, Policy Memo listing, for additional pseudo country codes

ATTACHMENT C - CANCELING FUNDS REPORT EXAMPLE

| Case | Country | Case Status |

Implemented Case Value |

Disbursements | Undisbursed Value | Date Closed or Estimated Closure Date |

Status/ Issues |

|---|---|---|---|---|---|---|---|

| $45,882,300.00 | $45,882,300.00 | $0.00 | Est. May 2011 (Green) |

|

|||

| $45,882,300.00 | $45,000,000.00 | $882,300.00 | Est. Jun 2011 (Yellow) |

|

|||

| $45,882,300.00 | $10,000,000.00 | $35,882,300.00 | Est. Sep 2011 (Red) |

|

|||

|

Please highlight accordingly |

|||||||

Key:

| Green - Low Risk of Not Closing by 31 July | Yellow - Medium Risk of Not Closing by 31 July | Red - High Risk of Not Closing by 31 July |

ATTACHMENT D - NOTIONAL TIMELINE

AUTHORIZATION THROUGH EXPIRING YEAR

| Frequency | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| On/ About |

Day | Week | Month | Tri- Annual |

Annual | Authorization Year through Expiring Year |

Expired Year +1 |

Expired Year +2 |

Expired Year +3 |

Expired Year +4 |

Canceling Year (Expired Year +5) |

Post Canceled Year |

|

| Obligate authorized/appropriated funding | 30-Sep | X | X | X | X | ||||||||

| Adjust obligations/expenditures | X | X | X | X | |||||||||

| DSCA to provide IAs with Pseudo LOA listing of all LOAs expired for obligation and subject to cancellation | 15-Nov | X | X | ||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 31-Jan | X | X | ||||||||||

| Submit new contract requiremens to IA; IAs begin writing LOAs | 10-Feb | X | |||||||||||

| Requirements submitted to IAs supported with existing contracts | 10-Mar | X | |||||||||||

| IA LOA manager completes and submits Pseudo LOAs to DSCA CWD for items not supported by existing contract | 10-May | X | |||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 31-May | X | X | ||||||||||

| IA LOA manager completes and submits Pseudo LOAs to DSCA CWD for items supported by existing contract | 10-Jun | X | |||||||||||

| DSCA to provide IAs with Pseudo LOA listing of those LOAs expired for obligation and subject to cancellation in the upcoming fiscal year | 15-Jun | X | |||||||||||

| Identify residual funding | 30-Jun | X | |||||||||||

| Contracting office receives Pseudo LOA/requirement for items not supported by an existing contract | 1-Jul | X | |||||||||||

| Contracting office receives Pseudo LOA/requirement for items supported by an existing contract | 1-Aug | X | |||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 30-Sep | X | X | ||||||||||

POST FUNDS EXPIRATION THROUGH YEAR OF CANCELATION

| Frequency | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| On/ About |

Day | Week | Month | Tri- Annual |

Annual | Authorization Year through Expiring Year |

Expired Year +1 |

Expired Year +2 |

Expired Year +3 |

Expired Year +4 |

Canceling Year (Expired Year +5) |

Post Canceled Year |

|

| Adjust obligations/expenditures | X | X | X | X | X | X | X | X | |||||

| IAs provide initial status of canceling cases to DBO-CFM | 1-Nov | X | X | ||||||||||

| DSCA to provide IAs with Pseudo LOA listing of all LOAs expired for obligation and subject to cancellation | 15-Nov | X | X | X | X | X | X | ||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-Dec | X | X | ||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 31-Jan | X | X | X | X | X | X | ||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-Jan | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 28-Feb | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-Mar | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 30-Apr | X | X | ||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 31-May | X | X | X | X | X | X | ||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-May | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 30-Jun | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 15-Jul | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-Jul | X | X | ||||||||||

| Liquidate all open funding lines | 31-Jul | X | X | X | X | X | X | X | X | X | |||

| IAs provide initial status of canceling cases to DBO-CFM | 15-Aug | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 31-Aug | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 7-Sep | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 14-Sep | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 21-Sep | X | X | ||||||||||

| IAs provide initial status of canceling cases to DBO-CFM | 30-Sep | X | X | ||||||||||

| Triannual Review - IAs review and reconcile commitments, obligations, accounts payable, and accounts receivable | 30-Sep | X | X | X | X | X | X | ||||||

POST YEAR OF CANCELATION

| Frequency | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| On/ About |

Day | Week | Month | Tri- Annual |

Annual | Authorization Year through Expiring Year |

Expired Year +1 |

Expired Year +2 |

Expired Year +3 |

Expired Year +4 |

Canceling Year (Expired Year +5) |

Post Canceled Year |

|

| Funds no longer available for any reason | X | ||||||||||||

| Triannual Review | X | ||||||||||||

* See guidance for notes concerning on/about dates