Superseded

SAMM Change has been superseded by DSCA 23-09.

Attachment 2 is incorporated into the DoD FMR Vol 3, Ch 8. Attachment 3 has been updated and is maintained by DSCA CMP A&R – dsca.ncr.obo.mbx.dar-q@mail.mil

| DEFENSE SECURITY COOPERATION AGENCY | 1/27/2021 |

MEMORANDUM FOR :

DEPUTY UNDER SECRETARY OF THE AIR FORCE FOR INTERNATIONAL AFFAIRS

DEPUTY ASSISTANT SECRETARY OF THE ARMY FOR DEFENSE EXPORTS AND COOPERATION

DEPUTY ASSISTANT SECRETARY OF THE NAVY FOR INTERNATIONAL PROGRAMS

DIRECTOR, DEFENSE CONTRACT MANAGEMENT AGENCY

DIRECTOR FOR SECURITY ASSISTANCE, DEFENSE FINANCE AND ACCOUNTING SERVICE - INDIANAPOLIS OPERATIONS

DIRECTOR, DEFENSE INFORMATION SYSTEMS AGENCY

DIRECTOR, DEFENSE LOGISTICS AGENCY

DIRECTOR, DEFENSE LOGISTICS INFORMATION SERVICE

DIRECTOR, DEFENSE REUTILIZATION AND MARKETING SERVICE

DIRECTOR, DEFENSE THREAT REDUCTION AGENCY

DIRECTOR, NATIONAL GEOSPATIAL INTELLIGENCE AGENCY

DEPUTY DIRECTOR FOR INFORMATION ASSURANCE, NATIONAL SECURITY AGENCY

DIRECTOR, MISSILE DEFENSE AGENCY

SUBJECT :

Dormant Account Review-Quarterly, DSCA Policy 20-83, SAMM E-Change 511

REFERENCE :

- Office of the Under Secretary of Defense (Comptroller), Dormant Account Review-Quarterly (FPM18-02) Policy, 20 August 2019

- Department of Defense Financial Management Regulation 7000.14-R, Volume 3 Chapter 8

Effective October 1, 2019, the Office of the Under Secretary of Defense (Comptroller) (OUSD(C)) policy referenced in (a), requires all DoD components to replace their Triannual Review process with the Dormant Account Review-Quarterly (DAR-Q) process. This change was implemented to demonstrate DoD's commitment to effective stewardship of financial resources through improved execution of budgetary resources, to include timely reconciliation and closure of Foreign Military Sales related financial transactions.

The DAR-Q policy serves as a quality control mechanism of entity-level internal control promoting accountability and corrective actions through follow-up on dormant financial transactions. Balances are defined as dormant if they have not been liquidated and no obligations, adjustments, contract modifications, disbursements, or withdrawals occur within the 90-day dormancy period. While this policy was effective across the DoD's Title 10 appropriated accounts, a consistent and effective review has not been performed for Title 22 Security Assistance Account (SAA) programs. In an effort to advance auditability of the SAA, it is critical that DoD Components perform this review within the prescribed timelines found in the DoD FMR 7000.14-R, Volume 3 Chapter 8.

Effective immediately, DoD Components executing Title 22 security assistance (SA) funds are required to comply with OUSD(C)'s DAR-Q guidance. DSCA acknowledges that the Air Force currently utilizes FM Suite to review dormant transactions, and plans to transition to the Advana platform in FY 2022. DSCA requests Air Force provide their transition plan to the Advana platform no later than August 2, 2021 to designated POC listed on this memo. To support the implementation of this policy, DoD Components should refer to OUSD(C)'s detailed guidance (attachment 2) and the SAA implementation timeline (attachment 3).

DSCA will maintain oversight and financial reporting of the SAA DAR-Q process. Additionally, DSCA will track compliance via quarterly metric reporting that will be used to monitor progress and/or address community-wide issues that may require senior leadership engagement. For any questions regarding this policy, please contact Ms. Raina Varghese at raina.varghese.civ@mail.mil or (202) 770-8594.

Jacqueline Leonard

Acting Chief Financial Officer

ATTACHMENTS :

- SAMM E-Change 511

- OUSD(C) Dormant Account Review-Quarterly (FPM18-02)

- SAA DAR-Q Implementation Timeline

Security Assistance Management Manual (SAMM), E-Change 511

Dormant Account Review Quarterly

1) ADD:

The Security Assistance (SA) community is required to follow Office of Under Secretary of Defense (Comptroller) (OUSD©) policy dated 20 August 2019, in which all DoD components are to replace the Triannual Review process with the Dormant Account Review-Quarterly (DAR-Q) process. This change was implemented to demonstrate DoD's commitment to effective stewardship of financial resources through improved execution of budgetary resources, to include timely reconciliation and closure of Foreign Military Sales related financial transactions. The DAR-Q policy serves as a quality control mechanism of entity-level internal control promoting accountability and corrective actions through follow-up on dormant financial transactions. Balances are defined as dormant if they have not been liquidated and no obligations, adjustments, contract modifications, disbursements, or withdrawals occur within the 90-day dormancy period. While this policy was effective across the DoD's Title 10 appropriated accounts, a consistent and effective review has not been performed for Title 22 Security Assistance Account (SAA) programs. DAR-Q is effective immediately for DoD Components executing Title 22 SA funds.

C14.4.1. FMS Case Reconciliation. The DAR-Q process will leverage existing internal control practices to assess whether commitments and obligations recorded are bona fide needs of the appropriations charged. Funds Holders, with assistance from supporting accounting offices, shall review financial dormant (inactive 90 days or more) transactions for timeliness, accuracy, and completeness during each DAR-Q review period ending March, June, September, and December. The DAR-Q process is a very effective tool in supporting the case manager's case management, reconciliation and closure responsibilities. Refer to DoD FMR, Volume 3, specifically Chapter 8 for additional policy information on the DAR-Q process.

2) REMOVE:

C16.2.3.2. Triannual Review. The Triannual Review process is an internal control practice used to assess whether commitments and obligations recorded are bona fide needs of the appropriations charged. Funds Holders, with assistance from supporting accounting offices, shall review dormant commitments, unliquidated obligation (ULO), accounts payable and accounts receivable transactions for timeliness, accuracy, and completeness during each of the four month periods ending on January 31, May 31, and September 30 of each fiscal year. The Triannual Review is a very effective tool in supporting the case manager's case management and reconciliation responsibilities. Refer to DoD FMR, Volume 3, Chapter 8 for additional policy information on the Triannual Review.

OUSD(C) Dormant Account Review-Quarterly (FPM18-02)

COMPTROLLER | OFFICE OF THE UNDER SECRETARY OF DEFENSE | 20 AUG 2019 |

MEMORANDUM FOR :

DEPUTY ASSISTANT SECRET ARIES OF THE MILITARY DEPARTMENTS (FINANCIAL OPERATIONS)

COMPTROLLER OF THE JOINT STAFF

COMPTROLLERS OF THE COMBATANT COMMANDS

COMPTROLLERS OF THE DEFENSE AGENCIES

COMPTROLLERS OF THE DOD FIELD ACTIVITIES

SUBJECT :

Dormant Account Review Quarterly (FPM18-02)

This memorandum replaces the existing Triannual Review with the Dormant Account Review Quarterly (DAR-Q) effective for all DoD components beginning Quarter (Q) 1, Fiscal Year (FY) 2020. The change exemplifies DoD's commitment to effective stewardship of taxpayer dollars through improved execution of budgetary resources. The amended review process reflects the Department's continuous improvement efforts and maturation of internal controls while enabling senior leadership to provide oversight and defend budgets.

Major updates, as detailed in the attachment, include a quarterly review of obligations and unfilled customer orders dormant over 90 days. The roles and responsibilities have been updated to promote accountability and corrective action follow-up. Populations and performance measurement have been realigned to improve budget execution, while record selection criteria emphasize high-risk and high-value balances.

The DoD Financial Management Regulation 7000.14-R, specifically Volume 3, Chapter 8, will incorporate this policy during the next update cycle. Additionally, the Office of the Deputy Chief Financial Officer's Chief Financial Officer Data Transformation Office has created an optional, automated tool within the Advana platform in which over 20 DoD entities executed their Q2, FY 2019 DAR-Q. Guidance and coordination will be provided as additional components transition to DAR-Q throughout FY 2019.

Thank you for your continued support of DoD financial improvement efforts. My point of contact for this effort is Ms. Elizabeth McEntire. Reach her at 703-614-1078 or elizabeth.t.mcentire.civ@mail.mil.

Mark E. Easton

Deputy Chief Financial Officer

ATTACHMENT :

As stated

Department of Defense Dormant Account Review -

Quarterly Transition Guidance -

August 2019

Dormant Account Review - Quarterly Goals

The Dormant Account Review - Quarterly (DAR-Q) serves as a quality control mechanism of entity-level internal control activities. In addition to providing the Office of the Under Secretary of Defense (Comptroller) (OUSD(C)) oversight, the DAR-Q improves the Department's ability to execute available appropriations before expiration and ensures remaining open obligations are valid and support accurate financial and budgetary reporting.

Automated DAR-Q tool

The OUSD(C) Chief Financial Officer Data Transformation Office (CDTO) collaborated with the Financial Improvement and Audit Remediation (FIAR) Directorate to design and launch an automated tool Components can utilize for performing the DAR-Q within the Advana platform. The tool leverages the DoD investment in the OUSD(C)'s universe of transactions to provide automated populations, reconciliations, record sampling, and a standard reporting platform. Performance of DAR-Q within Advana allows components to effortlessly adhere to policy requirements.

We conducted a pilot program in which five components reviewed their Q4, FY 2018 dormant accounts. Over 20 components, including the Marine Corps, executed their Q2, FY 2019 DAR-Q review within the tool. Throughout FY 2019, the CDTO and FIAR Directorates will support components' transition to DAR-Q through performance within the automated tool or implementation of internal procedures to meet unique business processes. To clarify, the tool was designed as an alternative solution and is not mandatory.

Populations

While respecting tie-points between proprietary and budgetary accounts, DAR-Q populations reflect the budgetary general ledgers impacting budget execution included on the table below.

DAR-Q Population | USSGL |

|---|---|

Undelivered Orders (UDO) | 4801, 4881, 4871, 4831 |

Delivered Orders, Unpaid (DOU) | 4901, 4981, 4971, 4931 |

UDO - Paid (UDOP) | 4802, 4882, 4872 |

Unfilled Customer Orders (UFCO) | 4221, 4222, 4230, 4253 |

Dormancy

DAR-Q only includes records with dormant balances. For purposes of the DAR-Q, current is defined as having a change in the status for obligations or unfilled customer orders during the last 90-day period, which generated general ledger activity. Balances are defined as dormant if they have not been liquidated and no obligations, adjustments, contract modifications, disbursements, or withdrawals occur within the 90-day dormancy period.

Review Periods

DAR-Q is a quality control mechanism to support the validity of balances reported on the quarterly financial statements. Therefore, review periods will occur during the quarter following the dormancy period.

Quarter | Dormancy Period | DAR-Q Review Period |

|---|---|---|

1 | October 1 through December 31 | January through March 20 |

2 | January 1 through March 31 | April through June 20 |

3 | April 1 through June 30 | July through September 20 |

4 | July 1 through September 30 | October through December 20 |

Sampling Methodology

DAR-Q sampling methodology focuses on high-risk, high-value balances. High-risk comprises dormant balances in expiring and canceling appropriations for General Funds and balances remaining after the period of performance has ended for Working Capital Funds and Foreign Military Sales. Populations are grouped by dollar value with higher sampling applied to high-value balances. Sampling methodology can be modified to reflect business events, such as continuing resolution authority, which impact budget execution timelines as well as consideration of qualitative factors, such as length of dormancy.

DAR-Q Roles and Responsibilities

Updated roles and responsibilities for the DAR-Q support quality control and accountability.

- Coordinator. Components are required to appoint at least one coordinator to serve as the OUSD(C) point of contact, disseminate records to appropriate personnel for review, and facilitate the DAR-Q process. Coordinators are not required to be financial managers, as their role is to facilitate the DAR-Q process by providing logistics, routing, and administrative support.

- Funds Holder. Funds Holders review dormant records to evaluate the status and initiate corrective action as necessary. Initiation of corrective action within ten business days, as well as monthly follow up until corrective action has been completed and general ledger posting has occurred, must be documented. Once the review is complete, records and supporting documentation are routed to their BSO for review.

- Budget Submitting Officer (BSO). BSOs use professional judgement to evaluate the appropriateness of the validation and sufficiency of the supporting documentation to provide reasonable assurance the Funds Holder completed their review in compliance with FMR policy and the Component's SOP requirements. BSOs must ensure Funds Holders have the capabilities to perform DAR-Q.

- Assistant Secretaries of the Military Departments for Financial Management and Comptrollers (FM&C). Comptrollers must establish Standard Operating Procedures (SOPs) for entity-level implementation of the DAR-Q, whether through utilization of the automated tool or manually through standard queries/reports, to ensure accuracy and completeness of the DAR-Q. Once the coordinator has consolidated all records, a certification statement will be signed by the comptroller prior to submission to OUSD(C) FIAR Directorate.

- OUSD(C) FIAR Directorate. FIAR will select a sample of Component's submission in order to perform quarterly review and provide feedback to assigned components. This oversight role includes monitoring performance, recommendation of best practices, and driving actions to achieve DAR-Q objectives.

- Service Providers and Sub-Allottees. Service providers and components who execute on behalf of others must provide documentation for sampled items as requested by their customers. The manner of customer requests, service provider response timelines and expected documentation types should be included within customer service agreements.

DAR-Q Validation

At a minimum, balances selected for review will be indicated as Valid, DAR-Q Adjusted, or DCAA/DCMA Review, defined below.

- Valid -A valid obligation where there is a reasonable likelihood that future activity will occur. Examples of activity include, but are not limited to, receipt of goods and services, payment of invoices, collecting payment for goods delivered or services rendered, or performing work on a reimbursable basis.

- DAR-Q Adjusted-A valid obligation that requires all or a portion of the balance to be adjusted in either the source General Ledger (GL) system or initiated with the responsible party (DFAS, Contracting Office, Performer, Source of Supply, etc.). An appropriate adjustment is any action required to adjust, the open balance to accurately reflect business events.

- DCAA/DCMA Review - A dormant balance that is currently under Defense Contract Audit Agency (DCAA) audit or Defense Contract Management Agency (DCMA) contract closeout procedures. Includes balances from contracts scheduled to be under DCAA audit or DCMA contract closeout procedures where the Agency no longer actively manages the open balance. Agencies must retain evidence that the open balance is currently under DCAA audit or DCMA has initiated contract closeout.

The automated tool allows users to select reason codes and provide additional granular data through explanation and comment fields. The collection of quantifiable data allows for analysis to ultimately drive decision making across the Department.

Key Supporting Documentation

OUSD(C) requires key supporting documentation (KSD) be provided for a sub-sample of DAR-Q records to support the balance, validation selected, and any corrective actions initiated. For dormant balances determined to be valid, documentation should support the remaining balance, while balances which require adjustment would include documentation to support the adjustment amount. KSD will be reviewed for quality control by OUSD(C)'s FIAR Directorate with feedback provided as necessary. The DAR-Q KSD requirement focuses on quality over quantity and supports future documentation requests as the Department continues the consolidated audit. When requested, KSD must be provided within 10 business days.

Standard Operating Procedures

Components are required to update Triannual Review SOPs (i.e., desk guides) to document entity-level DAR-Q procedures for implementation of the DAR-Q framework. For Components executing within the automated tool, SOPs should include internal timeframes to meet submission due dates and workflow descriptions which utilize the expanded process flow functionality. Components executing the DAR-Q outside the automated tool should include narratives documenting population generation, sample record selection, process timeframes, testing and reviewing procedures, and documentation requirements. The SOP should be written at the appropriate level of detail to allow an unfamiliar party to perform the appropriate steps without additional instruction.

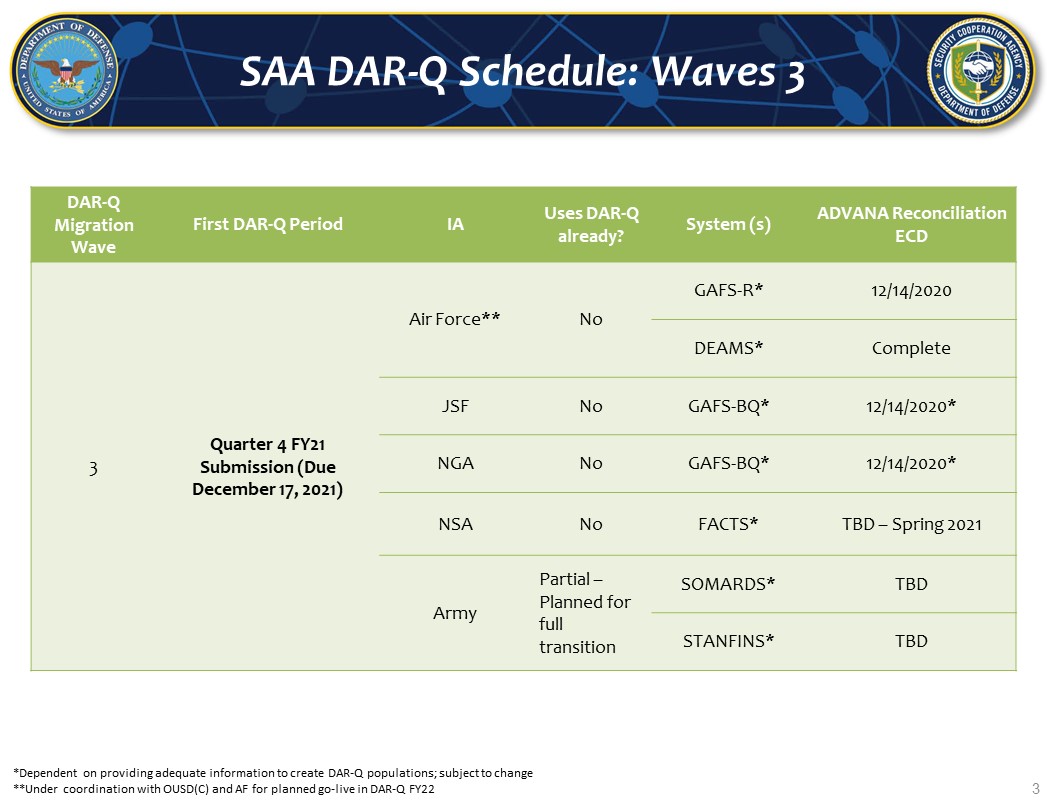

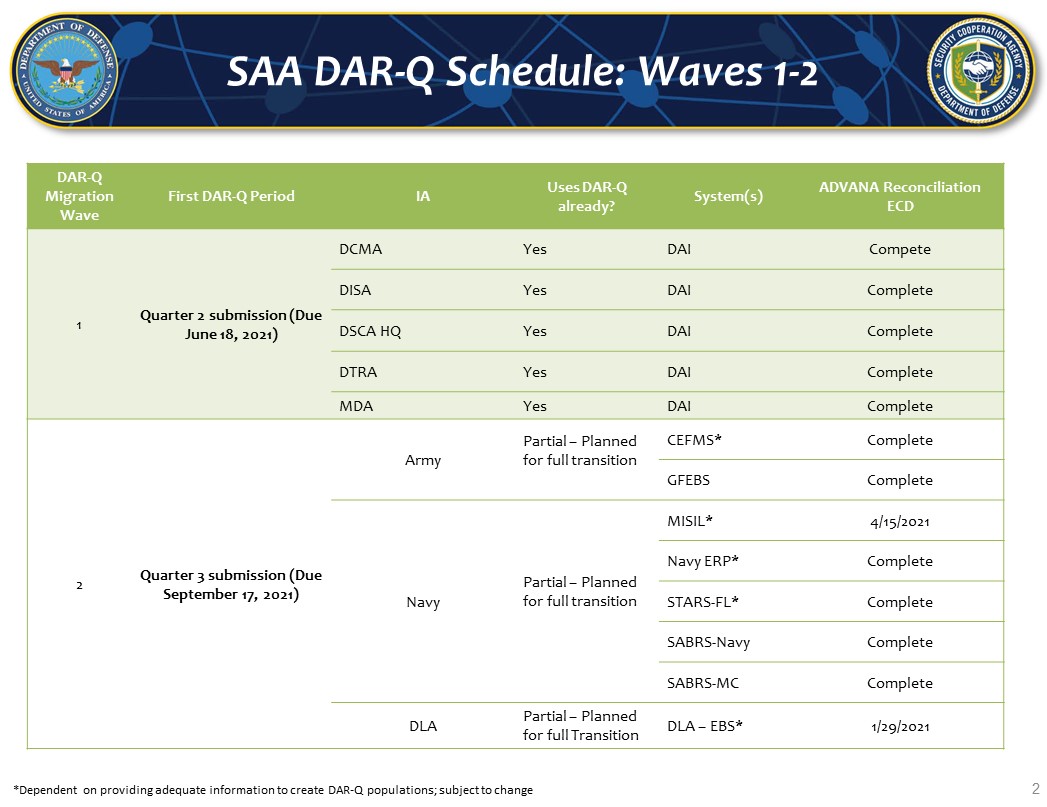

SAA DAR-Q Implementation Timeline

>

>