Chapter 4 outlines the closure process and includes information regarding certificate transactions and closure inhibitors once the certificate reaches Defense Finance and Accounting Service – Indianapolis (DFAS-IN). This chapter also documents the verifications required for post-closure transactions, contract closeout, the Case Closure Suspense Account (CCSA), reopening cases, zero value closures and closure of leases.

Section | Title |

|---|---|

AP7.C4.1. | |

AP7.C4.2. | |

AP7.C4.3. | |

AP7.C4.4. | |

AP7.C4.5. | |

AP7.C4.6. | |

AP7.C4.7. | |

AP7.C4.8. | Defense Integrated Financial System - Indianapolis Zero Case Closure Value Procedures |

AP7.C4.9. | |

AP7.C4.10. | |

AP7.C4.11. | |

AP7.C4.12. | |

AP7.C4.13. | |

AP7.C4.14. | Interim To Final Closure Processing For Accelerated Case Closure Procedure Cases |

AP7.C4.15. | Reopening And Reinstating Activity on Foreign Military Sales Cases |

AP7.C4.16. | |

AP7.C4.17. | |

AP7.C4.18. | |

AP7.C4.19. | |

AP7.C4.20. | |

AP7.C4.21. | |

AP7.C4.22. |

AP7.C4.1.1. Once a case is Supply/Services Complete (SSC) and the requisite verification steps noted in Appendix 7, Chapter 3, are completed, the case is eligible to be submitted for closure. As prescribed in the DoD Financial Management Regulation (DoD FMR), Volume 15, Chapter 6, a closed Foreign Military Sales (FMS) case may still remain open from a DoD accounting perspective. Case closure is the final phase of the FMS life cycle and is extremely important to the USG and purchaser. The benefits of case reconciliation and closure are numerous, but the most important benefit is that it ensures a country has received all the deliverables outlined in the FMS case, as well as, providing final billing and the return of any unutilized funds. Reconciliation for closure involves extensive communication between various logistics, financial and contract organizations to ensure associated closure transactions are completed. It is imperative that case/line reconciliation (elaborated in Appendix 7, Chapter 2 and Appendix 7, Chapter 3) is initiated upon implementation of the Letter of Offer and Acceptance (LOA) to ensure the closure process is overall less cumbersome. By reconciling during case execution, case closure becomes an event instead of a process. When a case is reconciled according to procedures for the appropriate closure method, it is then submitted for closure. This chapter addresses reconciliation surrounding the following processes: closure transactions, closure inhibitors, underpaid cases, Case Closure Suspense Account (CCSA), post closure transactions, verifications, contract closeout, reopening/reinstating activity, Foreign Military Financing (FMF) commitments, billing and lease closure.

The following serves as a general categorization of closure functions by organization:

AP7.C4.2.1. The Implementing Agency (IA) performs all case closure functions prescribed in DoD Financial Management Regulation (DoD FMR), Volume 15 and the SAMM, reconciles cases, ensures data integrity, performs annual case reviews and reconciliations in accordance with the requirements for closed cases as shown in Figure AP7.C2.F6., prepares cases for closure. For Accelerated Case Closure Procedure (ACCP) cases, to the maximum extent possible, this involves preparing the case for direct final ('C3') closure, coordinates internal case closure actions with appropriate organizations, issues the closure certificate and processes requisite closure transactions and analyzes cases for transition from interim to final (and final to interim) closure status, to include post-closure reconciliation efforts. In addition, the IA consults with Defense Finance and Accounting Service (DFAS), as appropriate, to ensure integrity between logistical and financial records, meets with purchasers to resolve issues, ensures closure status consistency between IA systems and Defense Integrated Financial System (DIFS), validates, liquidates, and adjusts the Unliquidated Obligation (ULO) value as appropriate and reopens Foreign Military Sales (FMS) cases as appropriate.

AP7.C4.2.2. DSCA is responsible for publishing, updating reconciliation and closure policies, and the master list of ACCP participants to include any special requirements for specific countries (See Table AP7.C3.T1. or the SAMM). DSCA oversees process of transitioning cases from interim to final closure, approves quarterly refunds from purchaser CCSA, serves as final arbiter for case closure issues raised by IAs and Defense Finance and Accounting Service - Indianapolis (DFAS-IN), provides approval for requests to reopen cases previously closed, and meets with purchasers to resolve issues.

AP7.C4.2.3. Defense Integrated Financial System - Indianapolis (DFAS-IN) works with IAs on closing cases, performs all accounting functions as prescribed in DoD FMR Volume 15 and the SAMM, meets with purchasers to resolve issues, collects final payments due from/refunds excess funds to purchasers, maintains the Case Closure Suspense Account (CCSA), effects quarterly ULO account refunds based on DSCA guidance, ensures prompt and accurate transition of cases between implemented and various closure categories, provides systemic feedback reporting to IAs, maintains case closure inventory in DIFS, reconciles financial data and validates FMS case closure values, closes FMS cases, ensures closure status consistency between IA systems and DIFS, reopens FMS cases, as authorized and reflects closure activity on DD Form 645, "Foreign Military Sales Billing Statement" and applicable holding account statements.

AP7.C4.2.4. Defense Contract Management Agency (DCMA), when assigned as the Administrative Contracting Officer (ACO), performs contract administrative functions (including contract closeout) as prescribed in the Federal Acquisition Regulation (FAR) and the Defense Federal Acquisition Regulation Supplement (DFARS).

AP7.C4.2.5. Defense Contract Audit Agency (DCAA) performs contract audit functions as prescribed in the FAR and the DFARS, including final overhead rate audits necessary to "final" close FMS cases.

AP7.C4.2.6. Purchasers advise IAs/DSCA on which cases are desired for closure, and those cases to be kept open, coordinate closure decisions between Ministry of National Defense (MND)/equivalent level and Service/program office level, and secure final payment in a prompt fashion for cases that are undercollected and awaiting closure.

AP7.C4.3.1. Tables AP7.C4.T1. and AP7.C4.T2. are checklists for preparation for Accelerated Case Closure Procedure (ACCP) interim to final closure (closure type '2' to '3') and for direct final closure of both non-ACCP closure type '1' and ACCP closure type '3'.

Table AP7.C4.T1. Checklist for Accelerated Case Closure Procedure Interim to Final Closure (Closure Type '2' to '3')

Click to view:

Table AP7.C4.T2. Direct Final Closure (Closure Type '1' and Closure Type '3')

To facilitate the closure of cases, depending on the closure type, the following are the steps applicable to determining the disposition of contracts and for contract closeout. Cases can be closed under limited circumstances, even if the supporting contract remains open (See Section AP7.C3.3.1.7.). Contracting functions are performed by the Administrative Contracting Officer (ACO).

AP7.C4.4.1. Time Standards. The target='_blank'>Federal Acquisition Regulation (FAR) Subpart 4.804 sets specific time periods for contract closeout. Only the ACO/Defense Contract Management Agency (DCMA) can enforce the time standards; the Implementing Agency (IA) has no authority to do so. The time period for contract closeout is based upon both the type of contract and date of physical completion. A contract is considered to be physically complete when the contractor has completed the required deliveries and the Government has inspected and accepted the supplies, performed all services and the USG has accepted these services, all option provisions, if any, have expired and USG has provided the contractor a notice of complete contract termination. Facilities contracts and rentals, use and storage agreements are considered to be physically complete when the USG has given the contractor a notice of complete contract termination and the contract period has expired.

AP7.C4.4.1.1. Files for contracts using simplified acquisition procedures should be considered closed out when the contracting officer receives evidence of receipt of property and final payment, unless otherwise specified by agency regulations.

AP7.C4.4.1.2. Files for firm-fixed-price contracts, other than those using simplified acquisition procedures, should be closed out within six months after the date on which the contracting officer receives evidence of physical completion.

AP7.C4.4.1.3. Files for contracts requiring settlement of indirect cost rates should be closed out within 36 months of the month in which the contracting officer receives evidence of physical completion. (Cost-Reimbursement Contracts including Time and Material (T&M) and Labor Hour (LH) contracts).

AP7.C4.4.2. Closeout of the Contract. If all contract terms and conditions are met, and all payments have been made to the correct ACRNs, the contract should be easy to close out and the process is completed.

AP7.C4.4.2.1. Following the FAR Subpart 4.804-5 "Procedures for Closing Out Contract Files", at the outset of this process, the ACO must review the contract funds status and notify the contracting office of any excess funds the contract administration office might de-obligate (Refer to the FAR Subpart 4.804-5 for a list of the actions required).

AP7.C4.4.2.2. Once all applicable actions are completed, the contracting officer administering the contract signs the Contract Closeout Checklist, if applicable.

AP7.C4.4.2.2.1. If the contract is in Mechanization of Contract Administration Services (MOCAS), the contracting officer also signs the Notice of Last Action (NLA) and processes the Final Payment NLA in MOCAS. MOCAS sends a contract completion statement (PK9) electronically to the contracting office and one is placed in the appropriate contract management office file.

AP7.C4.4.2.2.2. For contracts not in MOCAS, the ACO has to ensure that a contract completion statement (Defense Department (DD) Form 1594 "Contract Completion Statement") has been completed (Refer to the DCMA Contract Closeout Guidebook for details on preparing the form). For contracts not in MOCAS, the original contract completion statement must be sent to the contracting office and a copy placed in the appropriate contract administration file.

AP7.C4.4.3. Quick Closeout.The quick closeout procedures identified in FAR Subpart 42.708 offer an alternative to holding contracts open until the determination of final direct costs and indirect rates. When it becomes apparent that there is a delay in the settlement of final direct costs and indirect rates, it is recommended that the IA encourage the appropriate contracting officer to consider utilizing quick closeout procedures, where applicable. To help facilitate quick closeout, DCMA established a Contract Management Team (CMT) Locator hyperlink, as follows: https://pubmini.dcma.mil (USG Only). Specifically, quick closeout procedures may be used if the contract is physically complete and the amount of final direct and indirect costs to be allocated to the contract is relatively insignificant. Cost amounts will be considered relatively insignificant when the total unsettled direct costs and indirect costs to be allocated to any one contract, task order, or delivery order does not exceed the lesser of $1 million or 10 percent of the total contract, task order, or delivery order amount. The contracting officer is required to perform a risk assessment and determine that the use of the quick-closeout procedure is appropriate. The risk assessment shall include consideration of the contractor's accounting, estimating, and purchasing systems; other concerns of the cognizant contract auditors; and any other pertinent information. The determinations of final direct and indirect costs under quick closeout procedures are final for the contracts it covers and no adjustments are made to other contracts for over or under recoveries of costs allocated or allocable to the contracts covered by the advance agreement. Indirect cost rates used in the quick closeout of a contract are not considered a binding precedent when establishing the final indirect cost rates for other contracts.

AP7.C4.5.1. Contract Information Sources. When reconciling the status of a contract that relates to a Foreign Military Sales (FMS) case the information available may vary depending on when the basic contract was awarded or the FMS case start date. The following table provides an overview as to what case information is available at a particular point in the FMS case process.

Table AP7.C4.T3. Foreign Military Sales Case-Related Contract Information Sources

AP7.C4.5.2. Discontinued Research. An excerpt from the DoD Financial Management Regulation (DoD FMR) Volume 3, Chapter 11, addresses research requirements and provisions where discontinued research may be authorized. Efforts must first be made to obtain a final document status report regardless of the document type or the year of issuance. It is recommended that final documents are requested within six months after receipt of the material or work completion date has expired. This effort eliminates the possibility of reopening cases at a later date after unidentified charges are later located. The following procedures apply to closing out FMS contracts/funding documents when documentation to support the final expended value is no longer available.

AP7.C4.5.3. These procedures apply to cases funded with FMS and other appropriated funds. >Federal Acquisition Regulation (FAR) Subpart 4.804, provides time standards and responsibilities for closing out contract files. The Defense Contract Management Agency (DCMA) Guidebook outlines specific steps that must be taken prior to certifying the physical and financial completion of contracts by issuance of a Contract Completion Statement (Defense Department (DD) Form 1594/PK9 "Contract Completion Statement"). PCO, ACO and paying office records for many older contracts are incomplete or non-existent and records of contract closeout action are unavailable. The following policy guidance pertains to the removal of ULO balances in the official accounting system.

AP7.C4.5.3.1. Procedures and Requirements for Contracts Not Closed, but Physically Completed. For contracts requiring closeout in the payment system and/or accounting system, (e.g., Cost-Plus-Fixed-Fee and Fixed-Price-Incentive-Fee), perform the following, if possible:

AP7.C4.5.3.1.1. Complete the Contract Status Questionnaire shown in Figure AP7.C4.F1. to record/verify the current status of the contract; i.e., is the contract still open?; when shall the closeout process begin? If research reveals that the contract is not finalized, the questionnaire should remain with the investigating office. The questionnaire is intended to assist program offices in developing uniform procedures regarding contract status. Figure AP7.C4.F1. is intended to assist program offices in developing uniform procedures regarding contract status.

Figure AP7.C4.F1. Contract Status Questionnaire

AP7.C4.5.3.1.2. Obtain a Contract Completion Statement (DD Form 1594 or PK9) to confirm that the contract is closed out. Issuance of a DD Form 1594/PK9 does not signify that the contract is closed out in Mechanization of Contract Administration Services (MOCAS). Follow-up may be necessary in cases where the contract is still open in MOCAS to obtain status of pending audit and estimated close out date.

AP7.C4.5.3.1.3. Confirm accounting system obligations match contractual funding documentation for each Accounting Classification Reference Number (ACRN).

AP7.C4.5.3.1.4. Confirm accounting system disbursements match paying office, or when paying office records are not available, match to Treasury (Defense Cash Accountability System (DCAS)) disbursements for each ACRN.

AP7.C4.5.3.2. Procedures and Requirements for Closed Out Contracts vary based on the type of contract.

AP7.C4.5.3.2.1. On contracts for which required documentation to fully confirm contract closeout is unavailable, use the following approach to certify that closeout has been completed.

AP7.C4.5.3.2.2. For contracts requiring closeout in the payment system and/or accounting system, (e.g., Cost-Plus-Fixed-Fee and Fixed-Price-Incentive-Fee), accomplish the following if possible:

AP7.C4.5.3.2.2.1. Complete the Contract Status Questionnaire in Figure AP7.C4.F1. to record/verify the current status of the contract; i.e., if the contract still open or when shall the closeout process begin. Table AP7.C4.T4. shows the steps used to verify contract closeout. If research reveals that the contract is not finalized, the questionnaire should remain with the investigating office.

AP7.C4.5.3.2.2.2. Obtain a Contract Completion Statement (DD Form 1594 or PK9) to confirm that the contract is completed. Issuance of a DD Form 1594/PK9 does not signify that the contract is closed in MOCAS. Follow-up may be necessary in cases where the contract is still open in MOCAS to obtain status of pending audit and estimated close out date.

AP7.C4.5.3.2.2.3. Confirm that the accounting system obligations match contractual funding documentation for each ACRN and confirm accounting system disbursements match paying office records. When paying office records are not available, match accounting system disbursements to Treasury (DCAS) disbursements for each ACRN.

Table AP7.C4.T4. Steps Required To Verify Contract Closeout

# | Actions |

|---|---|

1 | Identify contractor, ACO, and paying office, using sources including:

|

2 | Determine closeout status. Sources for closeout information include MOCAS, ACOs/PCOs, Contractors and Contracts Directorate files. If a contract has been closed out, obtain documentation. The following hierarchy of acceptable documentation includes:

|

3 | If a contract has not been closed out - determine actions remaining before DD Form 1594 issued which may include:

|

4 | Use/maintain copies of Contract Status Questionnaire. |

5 | Determine contract financial closeout status:

|

6 | Submit Contract Status Certification (See Figure AP7.C4.F2.) to Comptroller and obtain concurrence. |

7 | Maintain copies of certifications in central file. |

Figure AP7.C4.F2. Contract Status Certification

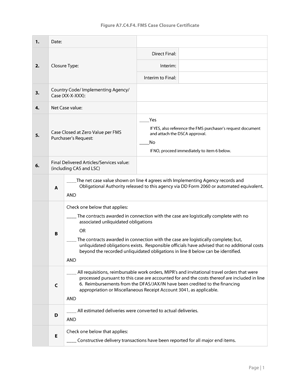

AP7.C4.6.1. With transmittal of the 'C1I' closure transaction (refer to Figure AP7.C4.F5.), the Implementing Agency (IA) submits the closure certificate via (format in Figure AP7.C4.F4.). For interim closures, the Unliquidated Obligation (ULO) supporting documentation attachment must be sent with the case closure certificate.

Figure AP7.C4.F3. Accelerated Case Closure Procedure Case Closure Preparation Actions for Cases with Unliquidated Obligations

Figure AP7.C4.F4. Foreign Military Sales Case Closure Certificate

Upon certification of the closure value, the 'C1I' closure transaction is generated by the Implementing Agency (IA) system and transmitted to Defense Integrated Financial System (DIFS) (Refer to Figure AP7.C4.F3.). The 'C1I' signifies IA completion of its actions necessary for Defense Finance and Accounting Service - Indianapolis (DFAS-IN) to close the case. This transaction is required for all closure submissions, except force closures.

AP7.C4.7.1. The 'C1I' transaction processes through the Positive Transaction Control (PTC) subsystem, invoking numerous edits and validations.

AP7.C4.7.1.1. Data Elements for the 'C1I' Transaction. The primary data elements are date submitted, case designator, certificate values including Contract Administration Services (CAS) and Logistics Support Charge (LSC) (at Interim closure, data elements include Unliquidated Obligation (ULO) and ULO CAS), articles/services disbursed (not including CAS or LSC) and closure type request code (Non- Accelerated Case Closure Procedure (ACCP) 'C1’, ACCP interim 'C2', or ACCP direct final or ACCP interim to final 'C3').

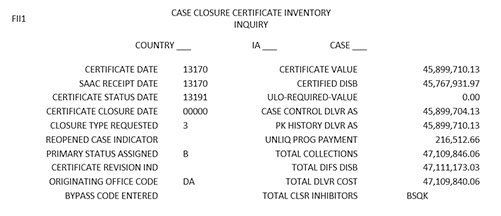

AP7.C4.7.2. The 'C1F' transaction is fed from DIFS to the IA system to acknowledge acceptance or rejection of the 'C1I'. If accepted by DIFS, the 'C1I' transaction is converted into a DIFS '2A' transaction resulting in a case closure certificate appearing on the Case Closure Certificate Inventory (CCCI) Inquiry screen (FII1). If rejected by DIFS, the IA receives a Transaction Reply Code (TRC) with the reason for rejection. In coordination with DFAS Indianapolis, the IA initiates whatever action is necessary to correct the condition before generating a new 'C1I' transaction.

AP7.C4.7.3. DIFS assigns closure status/inhibitor codes to all cases appearing on the CCCI. A list of DIFS inhibitor codes is provided in Table AP7.C4.T5.

AP7.C4.7.4. Each time a case closure certificate is added to the closure inventory for a ULO case, a new DIFS "ULO Required" value is computed as the difference between certified deliveries and the sum of certified disbursements and CAS/LSC disbursements in DIFS. This value is stored in the Case Control Summary Master File and appears in all Case Control Summary output and on the CCCI Inquiry screen. It is expected to support all post-closure financial activity reported against the case.

AP7.C4.7.5. Other Related Closure Transactions include the 'C4I', which is generated by the IA system to rescind the 'C1' transaction and related certificate of closure while the case is in pending closure status or prior to Defense Finance and Accounting Service (DFAS) closure approval, and the 'C5I', which serves two purposes:

- to reopen non-ACCP cases in DIFS and

- to revert cases from final to interim closure status (closure type '3' to '2').

The 'C5I' transaction is, generally, generated by the IA system and fed to DIFS. It is converted into a DIFS 'CF' transaction that changes the applicable case status in the Case Control Summary Master File of DIFS. The DIFS force closure 'C8' transaction is used to force close a case in DIFS.

AP7.C4.7.6. Once a case is closed in DIFS, a 'C3I' transaction is sent to the IA as notification that the case is closed in DIFS. Once all inhibitors are cleared in DIFS, a DIFS 'C8' transaction is submitted which closes the case in DIFS and sends a 'C3I' closure notification to the IA system. The IA system uses this transaction to update its closure status.

Figure AP7.C4.F5. C1/C3 Closure Transactions

Figure AP7.C4.F6. Defense Integrated Financial System Case Closure Certificate Inventory Inquiry

Upon case implementation, the Defense Integrated Financial System (DIFS) Admin Fee Subsystem transfers the required amount of the Foreign Military Sales (FMS) Administrative Surcharge (usually 50 percent) of the case FMS Administrative Surcharge ordered value from available funds in the Country Trust Fund to the FMS Administrative Surcharge Cost Clearing Account. This transfer is reflected on the Defense Department (DD) Form 645 as a portion of the Column 10, Work In Process. The presence of this progress payment on the Case Control Master File prevents the processing of a closure transaction (C8) for the cases closed at zero delivered value. When a cancellation fee is assessed for cases to be closed at zero delivered value, the system allows the case to be closed only if the ordered admin is reduced to equal assessed admin. Refer to Section AP7.C3.11. for a description of the process used to determine whether the case should close at a zero dollar value.

AP7.C4.8.1. Defense Finance and Accounting Service - Indianapolis (DFAS-IN) should not process zero case closure value requests unless they have been documented by DSCA in a Defense Security Assistance Management System (DSAMS) case remark and adequately documented as part of the case closure certification.

AP7.C4.8.2. For cases closed at zero delivered value without a cancellation fee, DFAS-IN processes a Change Case Detail ('CD') transaction to reduce the line level ordered admin cost to zero. This CD transaction causes the Admin Fee Subsystem to refund any money previously transferred and clears any 'progress payment admin'. As part of the 'CD' transaction, DFAS-IN includes Amend-Type 'C' and MOD-NBR '99', if the case has no previous closure actions to satisfy the requirements of the Case Amendment Control. If the case had a previous closure action, either do a correction to the C-99 line if adjustment is part of the original closure, or use C-98, 97, ext. as needed. DFAS-IN processes a 'CS' transaction to reduce case summary totals by the amount of admin reduced. The line level administrative surcharge percent established in Case Control is not changed or deleted. Upon successful processing of the 'CD' and "CS' transactions, a 'C8' transaction is processed to close the case.

AP7.C4.8.3. If the case is subsequently reopened, the 'CD' and "CS' transactions must be reversed to reflect the values on the Letter of Offer and Acceptance (LOA) in affect at the time of case closure.

AP7.C4.8.4. For cases closed at zero delivered value with cancellation fee, DFAS-IN processes an 'NF' flat charge transaction in the amount of the cancellation fee and closes the case in accordance with normal case closure procedures.

AP7.C4.9.1. Closure inhibitors applicable once the 'C1' transaction is sent to Defense Finance and Accounting Service - Indianapolis (DFAS-IN) are shown in Table AP7.C4.T5.

Table AP7.C4.T5. Defense Integrated Financial System Closure Inhibitors

AP7.C4.10.1. The Defense Integrated Financial System (DIFS) Case Closure Certificate Inventory (CCCI) reflects an 'L' inhibitor code whenever a case that is pending closure requires additional payment from the purchaser. Upon receipt of the closure certificate from the Implementing Agency (IA), Defense Finance and Accounting Service - Indianapolis (DFAS-IN) will issue an 'L’ inhibitor memorandum to the purchaser. This memorandum will detail the delivered and collected values, and the remaining amount due to close the case. Thereafter, DFAS-IN will send monthly notifications until the first quarterly billing statement (DD645) is issued following receipt of the closure certificate. If payment remains outstanding fifteen (15) days after the bill’s due date, DFAS-IN will generate a report of all 'Billed yet still Undercollected Cases' and submit it to the Defense Security Cooperation Agency (DSCA), specifically the Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE). In addition, DFAS-IN will add the CCCI inhibitor code to ‘D’ to indicate that responsibility for resolution resides with DSCA (OBO/FPRE).

AP7.C4.10.2. The Country Finance Director (CFD) will contact the partner as a final attempt to secure outstanding payment. In the event the purchaser does not remit payment within 90 days of CFD contact, DSCA may authorize the use of funds from the partner’s excess or residual trust fund balances to pay the outstanding amounts owed to clear the ‘L’ inhibitor. In addition, the CFD provides a final notice to partners that the amount due will be taken from excess and/or residual trust fund balances within 15 days. To facilitate the subsequent funds transfer, the CFD will also provide DFAS with the relevant partner correspondence, explicitly specifying the date and holding account from which the funds will be drawn. Once this information is received, DFAS-IN will independently confirm the amount due and then process the necessary transactions to transfer funds and satisfy the outstanding balances.

AP7.C4.11.1. When a case is being closed, any excess funds (as defined by collections less the closure value) are transferred by Defense Finance and Accounting Service - Indianapolis (DFAS-IN) to the appropriate holding account. National funds remain in the holding account unless/until the purchaser requests a transfer, refund or have an automatic refund arrangement in place. Generally, credit funds remain in the holding account until they are applied for required payments on other credit funded Foreign Military Sales (FMS) cases.

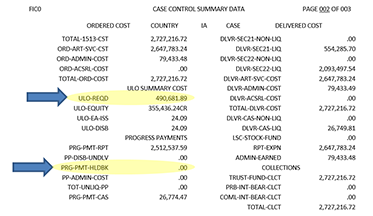

AP7.C4.12.1. Background. The Case Closure Suspense Account (CCSA) was established in 1992 with the onset of Accelerated Case Closure Procedure (ACCP). The account holds funds for all Implementing Agencies (IAs) for all participating countries and is maintained by Defense Finance and Accounting Service - Indianapolis (DFAS-IN) in Defense Integrated Financial System (DIFS) at country level and accounted for at case level. Prior to closure, the IA forwards the Unliquidated Obligation (ULO) value (including Contract Administration Services (CAS)) to DIFS (i.e., 'NA' performance transaction). The ULO value appears in the DIFS Case Summary query in the "ULO REQD" field at interim closure. The sum of "ULO-REQD" and "ULO-EQUITY" fields at case level equal the country level balances in the CCSA. See Figure AP7.C4.F7. for steps on how to update the CCSA. See Section AP7.C5.4. for additional information regarding the CCSA statement.

Figure AP7.C4.F7. Case Closure Suspense Account

AP7.C4.12.2. Defense Integrated Financial System Unliqudated Obligation Summary Costs. At interim closure, the total ULO certified value appears in the "ULO REQD" field found in DIFS Case Control Summary query. This amount is added to the CCSA country level balances. The "ULO REQD" amount is adjusted based on post closure Expenditure Authority (EA)/Disbursement activity. The "ULO DISB" is the liquidating costs received against the "ULO REQD" amount. The "ULO-EQUITY" field contains the amount of funds in the country level CCSA that had to be applied to the case to make up for a shortfall in the "ULO REQD" amount as a result of post closure EA/Disbursement activity against the case. The sum of "ULO-REQD" and "ULO-EQUITY" amounts for all cases is the available balance in the CCSA at the country level. The DIFS Case Control Summary fields show ULO summary costs on the DIFS Case Control Summary query in Figure AP7.C4.F8.

Figure AP7.C4.F8. Defense Integrated Financial System Case Control Summary Query

AP7.C4.12.3. Unliquidated Obligation Reporting Process. Incoming EA requests may either increase or decrease the CCSA balance. EA requests for credits will increase a CCSA balance while EA requests for debits will have a negative effect on the CCSA balance. Any unused ULO funds remain in the CCSA for subsequent use or refund. DFAS-IN monitors the account to ensure there are sufficient funds to process additional disbursements. Once the ULO is fully liquidated/de-obligated, the case can be submitted for final closure. DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE)) and DFAS-INreview the CCSA balances to determine if the country is eligible for a refund. Refer to Appendix 7, Chapter 5 for the CCSA statement lexicon and sample.

AP7.C4.12.4. Case Closure Suspense Account Refunds. The greater the accuracy of an original ULO estimates applicable to the case being interim closed under ACCP procedures, the less likely CCSA excesses result. Since the inception of ACCP, ULO estimates have not been exact, but, estimates have improved beginning in 2004 with the release of expanded ULO estimation policy. Once the case reaches final closure, any unused ULO value on the case is refunded by deposit into the appropriate holding account. The purpose of CCSA refunds are to release excess funds on deposit in that account as a result of activity against individual cases but based on the account value at the country level. This optimizes the utility of purchaser funds. The successful execution of CCSA refunds is dependent on a closely coordinated effort between DSCA (OBO/FPRE), DFAS-IN and IAs.

AP7.C4.12.4.1. Refunds are made on both interim closed and final closed cases. The process differs for each refund type.

AP7.C4.12.4.1.1. Interim Closed Cases. The process of reviewing for potential CCSA refunds occurs on a quarterly basis and refunds are processed before the end of the month in February, May, August, and November. IAs review proposed refunds on interim closed Foreign Military Sales (FMS) cases using the Interim Case Closure Refund tool in the Security Cooperation Management Suite (SCMS) and update recommendations for DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE)). DSCA (OBO/FPRE) provides a list of refunds to DFAS-IN with input from DSCA (Business Operations Directorate, Country Financial Management Division) and DFAS-IN (Customer Accounting Branch). DFAS-IN creates and processes the refund voucher and inputs the cash transfer transactions into DIFS to move excess funds to the appropriate holding accounts; posts the credit ULO EA adjustments to the corresponding cases; and processes corresponding progress payments at the line item level for each case that received a refund. The last action ensures that ‘ND’ performance reporting match disbursements to facilitate final closure.

AP7.C4.12.4.1.2. Final Closed Cases. The process for reviewing for potential CCSA refunds occurs on a quarterly basis and refunds are processed before the end of the month in March, June, September, and December. DFAS-IN provides various reports and data to DSCA (OBO/FPRE) on ULO balances. DSCA (OBO/FPRE) forwards to and DFAS-IN its comprehensive report, produced by the DSCA Final Closed Case Refund tool, identifying all countries for which excess CCSA funds appear to exist, along with its recommendation on the excess funds eligible for refund. The report details the specific cases comprising the country-level CCSA excess funds total. DSCA (OBO/FPRE) and DFAS-IN review and coordinate on the identified refunds. DSCA (OBO/FPRE) provides direction to DFAS-IN on the amount of CCSA refunds. Due to limitations within DIFS, DFAS-IN temporarily moves the case to an interim closure status (‘C2’) which allows for transactional processing of refunds. However, before such action is taken, DFAS-IN reviews the suspended transaction file and removes any transactions that would impact the movement of the case back to final closure status (‘C3’). DFAS-IN then creates and process the refund voucher and inputs the cash transfer transactions into DIFS to move excess funds to the appropriate holding accounts; processes corresponding progress payments at the line item level for each case that received a refund; and returns the case to a final closure status (‘C3’).

AP7.C4.12.4.2. Disposition of funds originating from cash-funded cases requires DFAS-INto transfer funds originating from cash-funded to the FMSTrust Fund holding account 7QQ. This holding account serves as a temporary repository of those funds and provides an appropriate audit trail for monitoring CCSA refunds. DSCA (OBO/FPRE) requests that purchasers respond within a reasonable time frame with their authorizations to transfer these funds to more desired repositories. Options for disposing of these funds include: cross-leveling to active FMS cases for the purpose of liquidating arrearages or minimizing future outlay requirements; transferring to other holding account(s), perhaps for the purpose of further segregating excess funds by In Country Service (ICS) and/or refunding directly to the purchaser.

AP7.C4.12.4.3. Disposition of funds originating from FMS Credit and Military Assistance Program (MAP) Merger-Funded cases begins when DFAS Indianapolis transfers the refunds to the ‘5QQ’ (Credit) or ‘2QQ’ (MAP Merger) holding account, whichever is identified in the comprehensive refund report. DSCA (OBO/FPRE) records into the FMS Credit System database an offsetting commitment entry (i.e., a negative ‘RA’ transaction) using pseudo case identifier Q-ULO as the audit trail for monitoring these transactions. This action increases the purchaser’s Foreign Military Financing (FMF) uncommitted balance by a corresponding amount. Funds are de-committed from pseudo case Q-ULO to finance Letters of Offer and Acceptance (LOAs) as they are presented for funding.

AP7.C4.12.4.4. Refunds are reflected in the purchaser’s applicable holding accounts statements and the CCSA statement provided with the quarterly DD Form 645, “Foreign Military Sales (FMS) Billing Statement”.

AP7.C4.13.1. Interim Closure Status. Once the case has reached interim closure (closure type '2') status, only obligation ('R' series) work in process performance reporting 'ND' and disbursement/ Expenditure Authority (EA) ('S' series) transactions relating to post-closure charges can process (Refer to Figure AP7.C4.F9.). All delivery performance ('NA') transactions shall reject during interim closure. Accelerated Case Closure Procedure (ACCP) allows charges that exceed the Unliquidated Obligation (ULO) to process programmatically (certain restrictions apply for individual ACCP participating countries). When charges exceed the ULO value assessed at interim closure by $100,000 or more or they will reduce the Case Closure Suspense Account (CCSA) balance of the purchaser by more than 75 percent, DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate, Financial Policy Division (OBO/FPRE/FP)) may authorize the case to be reopened in order to process the additional charges. Based on the specific transaction, funds may be withdrawn from or deposited into the CCSA (refer to additional details in Appendix 7, Chapter 5). Table AP7.C4.T6. illustrates transactions to process charges received while a case is interim closed:

Table AP7.C4.T6. Post-Closure 'ND' Performance Transactions

Contract Related | Performance Transaction | Price Code | Delivery Source Code | Reimbursement Code | Contract Administration Services | Defense Integrated Financial System |

|---|---|---|---|---|---|---|

Yes | 'ND' | N | DE | D | Yes | Progress Payment Reported |

No | 'ND' | Blank | DF | S | No | Progress Payment Reported |

Figure AP7.C4.F9. ‘ND’ Post Closure WIP Performance Transaction Processing

AP7.C4.13.2. Final Closure Status. For processing additional disbursement, obligation and expenditure authority transactions, ACCP cases previously in final closure status (closure type '3'), must revert to interim closure status (closure type '2'). When charges exceed the ULO value assessed at interim closure by $100,000 or more or they will reduce the CCSA balance of the purchaser by more than 75 percent, the IA shall consult with DSCA (OBO/FPRE/FP) before moving a case to interim closure status. DSCA will determine if the Implementing Agency (IA) should proceed with the closure type change or if the case should be reopened. Any non-ACCP transactions require the case to be reopened.

AP7.C4.13.3. Post Closure Supply Discrepancy Reports. All case closure types require that any Supply Discrepancy Reports (SDRs) be finalized prior to submitting a case for closure. (Refer to the SAMM Chapter 6, for detailed policy guidelines on SDRs.) However, while it is rare, SDRs may be received after a case is closed. Post-closure SDRs must be validated and approved by the normal SDR approval authority prior to any further action on the closed case (Refer to Figure AP7.C4.F10.). An SDR received against a closed case is processed as follows:

AP7.C4.13.3.1. Accelerated Case Closure Procedure Cases. Valid SDRs will be processed against interim closed cases (closure type '2'). A final closed case (closure type '3') must revert to interim closure status to process an SDR. Defense Integrated Financial System (DIFS) accepts only 'ND' and 'S' series transactions during interim closure. After the SDR processes, the 'ND' performance transaction draws from or is applied to the CCSA (credits return funds to the CCSA; debits withdraw funds from the CCSA). Upon completion of SDR actions, and provided all other inhibitors are cleared, the case may be final closed.

AP7.C4.13.3.2. Non- Accelerated Case Closure Procedure Cases Cases must be reopened to process an SDR. Normal processing of the SDR occurs once the case is returned to an "implemented" status. An 'NZ' SDR transaction is forwarded to report the SDR to Defense Finance and Accounting Service - Indianapolis (DFAS-IN) and is recorded in DIFS. Upon completion of the SDR actions, the case can be re-closed.

AP7.C4.13.3.3. Submittal of Supply Discrepancy Reports. The Military Department (MILDEP) points of contact for receipt of SDRs are:

MILDEP | Address |

|---|---|

Army | U.S. Army Security Assistance Command (USASAC) 54 M Avenue, Suite 1, New Cumberland, PA 17070-5096. |

Navy | Naval Supply Systems Command (NAVSUP) Weapons System Support Deputy Commander for International Programs 700 Robbins Ave, Bldg 4B, Code N5232, Philadelphia, PA 19111-5098. |

Air Force | Air Force Life Cycle Management Center (AFLCMC)/WFIUB 5454 Buckner Rd, Wright-Patterson Air Force Base (WPAFB), OH 45433-5337. |

Figure AP7.C4.F10. Supply Discrepancy Report Processing Against Closed Cases

AP7.C4.14.1. In those instances where a case must first close in an interim closure status, it is important that they are monitored on a continual basis to progress the case to a final closure status as early as possible.

AP7.C4.14.2. Review of Defense Integrated Financial System (DIFS) case summary includes the review of all payments and funds receipts. A DIFS case summary review will show the case as closure type '2', for interim closed. To consider a case for final closure the review must include the DIFS values and associated Implementing Agency (IA) systemic balances, the contract status/type, receipt of all final disbursements, review of all remaining values (to include Obligational Authority (OA)), progress payments reported ('ND' transactions), post closure problem disbursements, cost closure Supply Discrepancy Reports (SDRs), Case Closure Suspense Account (CCSA) refund that may have occurred and a validation of accessorial charges.

AP7.C4.14.3. Review Unliquidated Obligation (ULO) data and take any necessary actions to liquidate or deobligate any unneeded amount in the IA systems.

AP7.C4.14.3.1. When refunds occur during interim closure, certain variances will result on the case. Specifically, interim refunds will cause progress payments to exceed liquidating deliveries by the amount of the interim refund. In addition, interim refunds will result in a disbursement variance between DIFS and the IA by the amount of the refund. These conditions should be taken into consideration when certifying an interim closed case for final closure. However, these specific conditions should not prevent the final closure certification of the case.

AP7.C4.14.4. In order to verify contract/other funding document status the reviewer must review ULO supporting documentation provided with interim closure certificate (Refer to Figure AP7.C4.F4.), review the entitlement system (e.g., Mechanization of Contract Administration Services (MOCAS)), contact the case manager (CM)/ Case Administering Office (CAO), Administrative Contracting Officer (ACO) or Procuring Contracting Officer (PCO) to obtain date for finalization of contract/other funding document (Refer to Table AP7.C4.T3. for an inventory of possible sources), and ensure obligations are posted in accordance with the contract/other funding document. If obligations were not posted and the additional obligations exceed $100K, the case may need to be reopened. In addition the reviewer must obtain the amount of final expenditure for each Accounting Classification Reference Number (ACRN) on the contract/other funding document. Obtain the date when final expenditures are expected or were incurred.

AP7.C4.14.5. DIFS Performance reporting during interim closure will not accept 'NA' (delivery) as well as Logistics Support Charge (LSC) and liquidating Contract Administration Services (CAS) (NA) performance transactions. However, 'ND' transactions reflecting work-in-progress and progress payment CAS, as well as, obligations ('R' series), and disbursements ('S' series) will continue to process. Prior to final closure all performance rejects must be cleared. CCSA adjustments (including credits/SDRs) will occur via the 'ND' performance and 'S' series transactions.

AP7.C4.14.6. Post-interim closure expenditures can be less than, greater than or equal to the ULO estimate calculated at interim closure. If no ULO exists and expenditures are greater than or less than the remaining program value by $100K, request DSCA written permission to reopen the case and process a LOA modification. Reopening procedures are discussed in Section AP7.C4.15.

AP7.C4.14.7. To validate obligations reported to DIFS, the reviewer must review DIFS (FIF2) obligations, resolve all outstanding reporting differences and adjust obligations (i.e., de-obligate) in the IA systems, if necessary.

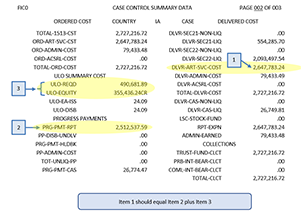

AP7.C4.14.8. To validate performance values DIFS delivered articles and services value must equal IA performance values. (The formula: Add articles/services expenditures plus Estimated ULO CAS and LSC/Stock Fund expenditures, then subtract ULO CAS costs and any ULO adjustment amounts.) For DIFS performance to match, liquidating deliveries must equal progress payments, or the difference equates to the unused ULO (ULO-REQD plus ULO-Equity). See Figure AP7.C4.F11. In this example, item 1 equals item 2 plus item 3.

Figure AP7.C4.F11. Defense Integrated Financial System Performance Reconciliation

AP7.C4.14.9. Validate DIFS disbursement values by ensuring DIFS cash accounting and articles/services disbursement values equal IA performance values. Compare DIFS cash accounting CAS, LSC, ULO, accessorial and administrative disbursement transfers to case summary values. Total deliveries (DIFS FIC1) less total disbursements (DIFS FIS2) must equal ULO-REQD value. If a CCSA refund will be given, or was recently given, to the purchaser, this may cause a disbursement difference between DIFS and the IA system, as well as Work-in-Process versus Deliveries difference with the same dollar amount. However, the two differences should not prevent final closure.

AP7.C4.14.10. Validate remaining ULO values by researching and documenting LOA line numbers, funding documents, requisition numbers, articles/services obligated value, articles/services expended value, ULO value (excluding CAS) and the reason for ULO. It is important to note that the following information mirrors the ULO supporting documentation section of the interim case closure certificate as noted in Figure AP7.C4.F4., provided earlier in this chapter. If no ULO remains, proceed to remaining steps in this section. If valid ULO remains, the case must stay interim closed.

AP7.C4.14.11. To submit a case for final closure the IA forwards the case for closure when the case is both logistically and financially complete. The steps noted in Section AP7.C4.14.2. through Section AP7.C4.14.10. above must be completed. Following completion of those steps the IA sends 'C1' transaction to DIFS, IA sends final case closure certificate to Defense Finance and Accounting Service (DFAS) (Refer to Figure AP7.C4.F4. of this chapter for the case closure certificate format), the case closure certificate is approved by DFAS and final closed in DIFS, DIFS closure type transits to '3', and DIFS sends a 'C3' transaction to IA system. This prompts the case to be closed in the IA system. After final closure, DIFS will not accept any further transactions, other than the 'C5' (case reopen) transaction.

Reopening a closed Foreign Military Sales (FMS) case is performed on an exception basis only. Reinstating activity applies to a case not yet closed, but which is in the closure process or, at a minimum, is not currently active from a logistical perspective. The following describes the reopening and reinstating processes. Cases may be reopened or reinstated for additional processing, e.g., disbursements or Supply Discrepancy Reports (SDRs). Figure AP7.C4.F12. and Figure AP7.C4.F13. illustrate these concepts.

AP7.C4.15.1. Reopening Foreign Military Sales Cases. In general, reopening for the purpose of resuming logistical activity is discouraged. Normally, either establishing a new case or amending an existing case is preferred. The purchaser (normally, an official with at least Letter of Offer and Acceptance (LOA) signature authority; but higher approving authority may exist) must confirm that reopening the FMS case is the only viable course of action. Also, there are situations when a case must be reopened to process valid financial transactions. When it appears that the correct course of action is to reopen a FMS case, the IA must send a written request (e-mail), through the Implementing Agency (IA) focal point for case closure, when one exists, to DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate, Financial Policy Division (OBO/FPRE/FP)) for approval. If the request action is denied, the case shall remain closed. If the requested action is approved, the IA coordinates with Defense Finance and Accounting Service - Indianapolis (DFAS-IN) to reopen the case and also advises the purchaser of reopening criteria (e.g., the timeframe in which activity must resume). Reopening allows a case to be returned to an implemented status or reverted to interim status in order to process additional disbursements/SDRs.

AP7.C4.15.1.1. The 'C5' case reopen transaction is used by the IA to either reopen non- Accelerated Case Closure Procedure (ACCP) final closed (closure type C1) cases to implemented status; reverse ACCP final closed (closure type C3) cases to an interim closed status (closure type C2); or with DSCA approval move an ACCP interim closed case to implemented status. If an ACCP case is final closed, two consecutive 'C5' transactions are necessary to move the case to implemented status. The 'C5' transaction may take up to two working days to process in DIFS. The 'C5' transaction includes the date on which the case was reopened.

AP7.C4.15.1.2. Reopening a final closed case to an implemented status is done manually by DFAS-IN upon DSCA (OBO/FPRE/FP) approval of an IA request if the IA cannot perform this function via the submission of a C5 transaction.

AP7.C4.15.1.3. Once a case is re-opened and returns to implemented status, generally, a 'C4' transaction is submitted to cancel the closure certificate record in the Defense Integrated Financial System (DIFS) Case Closure Certificate Inventory (CCCI). This is necessary as any additional financial activity will require the submission of a new closure certification.

AP7.C4.15.1.4. For additional processing against ACCP cases, a Direct Final or Final after Interim closed case returns to interim closure status. However, when charges exceed the Unliquidated Obligation (ULO) value assessed at interim closure by $100,000 or more or they will reduce the Case Closure Suspense Account (CCSA) balance of the purchaser by more than 75 percent, the IA shall consult with DSCA (OBO/FPRE/FP) before moving a case to interim closure status. DSCA will determine if the IA should proceed with the closure type change or if the case should be reopened.

AP7.C4.15.2. Once all charge processing is complete, the case may be resubmitted for closure via a 'C1' transaction. A revised certificate is required.

Figure AP7.C4.F12. Reopening and Reinstating Activity on Foreign Military Sales Cases

Figure AP7.C4.F13. Reopening a Closed Case/Reverting from Final to Interim Closure

AP7.C4.15.3. Reinstating Activity. Reinstatement allows a case that is pending closure to return to its previous status. The process for reinstating activity on cases differs, depending on the status of the case when the reinstatement request is received from the FMS purchaser (Refer to Figure AP7.C4.F14.).

AP7.C4.15.3.1. If the case is at DFAS-IN for closure (i.e., it is recorded in the DIFS case CCCI, reinstatement is generally discouraged. By this juncture, the case already has been in the closure process for quite some time; for this reason, other alternatives such as using another case must be considered. The purchaser (normally, an official with at least LOA signature authority; but, higher approving authority may exist) must confirm that retraction of the closure certificate is desired. If the purchaser confirms that reinstatement is the solution, the IA must send a written request (e-mail) to DSCA (OBO/FPRE/FP) for approval to cease closure actions and to allow for activity to resume. If the request is denied, closure actions shall proceed. If the request is approved, the IA retracts the closure certificate from DIFS. The IA then advises the purchaser of reinstatement criteria (e.g., the timeframe in which activity must resume).

AP7.C4.15.3.2. The 'C4' cancel closure certificate transaction is used by the IA to rescind/cancel an active case closure certificate before the case is actually closed by DFAS-IN. When the 'C4' transaction processes, the DIFS CCCI record is deactivated and removed from the active CCCI, and the computed ULO-REQD value is zeroed out in DIFS. At this point, the IA should reverse any ULO 'NA' deliveries previously submitted. Once a case is closed in DIFS, the certificate cannot be rescinded or cancelled; the case must be reopened. Further, if an interim closed case is certified for final closure, the final closure certificate cannot be cancelled. Instead, the case must be final closed, then the IA may submit a 'C5I' transaction to revert the case status to interim closed. This action causes a cancellation of the final closure certificate.

AP7.C4.15.3.3. If the case is not at DFAS-IN for closure, the IA decides whether to approve the purchaser's request. If the IA denies the request, actions continue to prepare the case for closure. If the IA approves the request, the purchaser is notified accordingly and provided conditions, if appropriate (e.g., the timeframe for resumed activity).

Figure AP7.C4.F14. Cancelling a C1I Closure Transaction

When a case is received into the Defense Integrated Financial System (DIFS) Case Closure Certificate Inventory (CCCI), Defense Finance and Accounting Service - Indianapolis (DFAS-IN) verifies the funding source(s) for the case. If Foreign Military Financing (FMF) (Foreign Military Sales (FMS) Credit, FMS Credit (non-repayable), and/or Military Assistance Program (MAP) Merger) was reserved for the case, DFAS-IN must coordinate adjustments to the FMF commitments with DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE)). An FMF-financed case is not considered closed for accounting purposes until the commitment adjustment process is completed.

AP7.C4.16.1. DFAS-IN sends a request to the DSCA (OBO/FPRE) for a commitment adjustment to the FMF-financed case awaiting closure. The request should not be made until the CCCI status for that case is 'I', indicating that no further reconciliation issues are anticipated. If the CCCI status is other than 'I', that indicates that additional reconciliation actions should occur, thereby making the commitment request premature.

AP7.C4.16.2. DSCA (OBO/FPRE) confirms that the revised commitment value equals the anticipated closure value. If the case is partially financed with FMF the revised commitment value must equal the final FMF collections as recorded in DIFS. The FMF commitments are then adjusted for that case. DSCA (OBO/FPRE) consults with DFAS-INif any imbalances or other problems arise that preclude the adjustment transaction. For example, if the FMF commitments must increase to reflect the closure value, yet insufficient FMF funds remain, DSCA (OBO/FPRE) must coordinate actions with the purchaser. (At times, those actions may result in other cases being de-committed to avail sufficient funds for the case being closed. At other times, the purchaser may have to remit cash to cover the funding shortfall.)

AP7.C4.16.3. DSCA (OBO/FPRE) sends a written notice (usually via e-mail) to DFAS-INconfirming the commitment actions taken.

Closure of a case impacts the official billing statements sent by the USG to the purchaser. Discussion of its impact on the Defense Department (DD) Form 645 (Foreign Military Sales Billing Statement) and Special Billing Arrangement (SBA) is contained below.

AP7.C4.17.1. Impact on the Defense Department Form 645. The DD Form 645 is sent quarterly to all purchasers. When a case has been closed during the quarterly period covered by an individual billing statement, an asterisk (*) appears to the left of the case designator. This indicates that the case was closed during that quarter. If residual funds were realized at the time of closure, or if funds were transferred to the case so that collections equaled the case value, those transactions appear on the appropriate holding account statement. Refer to the DD Form 645 sample in Figure 6-3 of the Security Cooperation Billing Handbook (The Red Book).

AP7.C4.17.2. Impact on the Special Billing Arrangement. Normally, the SBA does not contain any closure information. An exception is if a case is pending closure at Defense Finance and Accounting Service – Indianapolis (DFAS-IN), but additional funds are needed from the purchaser to align collections with the case closure value. In this instance, the SBA cites the cases and payment amounts needed for closure to occur. This information should be gathered by DFAS-INand transmitted to DSCA (OBO/FPRE) as the SBA is being prepared for issuance. Usually, amounts needed to close cases are additive to the calculations for working capital requirements for the period covered by the SBA.

The authority for leases is contained in Section 61 of the Arms Export Control Act (AECA) (22 U.S.C. 2796). Please refer to Appendix 8, Lease of Defense Articles for detailed lease program information. The administration of leases is delegated to the Implementing Agency (IA) logistically responsible for the defense articles being leased. It is necessary for each IA to ensure that leases under their cognizance are properly closed. A lease cannot be closed until the equipment is returned, all related costs are recovered under Foreign Military Sales (FMS) procedures (such as costs for restoration), and the lease rental payments are paid in full.

AP7.C4.18.1. If a lease expires and the leased material has not been returned, there is no mechanism in place by which the USG can recoup the rental payments not being collected. The lease must be extended prior to lease expiration if an item is to remain in country after expiration of the lease. This allows the USG to charge rental payments to the leasing party and to ensure that the country remains bound to the legal terms and conditions of the lease.

AP7.C4.18.2. Ifa lease expires and the material is returned or disposed of, but the rental payments have not been paid in full, the lease cannot be closed. The IA must ensure that the lease is financially closed. The IA should work with Defense Finance and Accounting Service – Indianapolis (DFAS-IN) and DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE)) to resolve outstanding payments.

AP7.C4.18.3. Section 61 of the AECA (22 U.S.C. 2796) states that leases "shall be for a fixed duration of not to exceed five years." If the lease is not closed within five years of the date the lease was implemented, the IA is in violation of this statute.

AP7.C4.18.3.1. In the event a lease is not closed within five years of the date the lease was implemented, the IA must prepare a new lease to recoup the additional depreciation charges that accrue for the duration the equipment remains in country after the expiration date of the original lease.

AP7.C4.18.4. Section 62 of the AECA (22 U.S.C. 2796a) states that Congress must be notified of "any agreement with a foreign country or international organization to lease any defense article... for a period of one year or longer." If a lease with a duration of less than one year is not properly closed, and no action is taken to extend the lease (to include proper coordination and congressional notification), the IA is in violation of this statute.

AP7.C4.18.4.1. In the event a lease with a duration of less than one year is not properly closed, the IA must prepare a lease amendment to recoup the additional depreciation charges that accrue for the duration the equipment remains in country after the expiration date of the original lease and request DSCA (Office of International Operations, Global Execution Directorate, Assistance & Monitoring Division (IOPS/GEX/AMD)) notify congress of the lease amendment.

AP7.C4.18.5. The IA is responsible for the following lease closure actions:

AP7.C4.18.5.1. Lease closure procedures shall begin at least two quarters prior to the expiration or termination of the lease. Management Flags are generated by the Defense Security Assistance Management System (DSAMS) to the Lease Case Manager prior to the lease expiration date (180 days, 90, 60, 30), when the lease is Expired, and 30, 60, 90, 120 and 180 days following Lease Expiration. The 'post-expiration' flags are generated unless the Lease has been closed.

AP7.C4.18.5.2. Arrangements for return (to include restoration to original condition) or disposal of the leased material shall be completed prior to the expiration of the lease.

AP7.C4.18.5.3. Upon return of the items to U.S. custody, the IA posts the item Actual Return Date for each Lease Line in DSAMS. Once all line items have been returned and inspected, the Lease Detail window Lease Tab (I version) should be updated to indicate all items have been returned. Select "subject-open-lease-detail" (I version) and enter the Actual Return date in the Shipment Tab. The Lease Detail Actual Return Date is the date that appears in the DSCA Quarterly Report. The IAs are responsible for entering the Actual Return Dates to both the Lease Line window and the Lease Detail window (when all lines have been returned).

AP7.C4.18.5.4. All rental payments and related costs must be collected before lease closure. A notification needs to be made to Defense Finance and Accounting Service (DFAS) when the items are returned so that DFAS-IN can initiate financial closure of the Lease. In DSAMS, select "subject-open-lease-detail," enter the lease designator (I version) and go to the Lease Tab. Select "Tools-Update Implemented Lease". Click on the Text Type Add button and select DFNOT from the drop down list. Enter a title "DFAS Notification" and enter a date in the comments field. ONLY a date should be entered, e.g., 1 Dec 2003. Once the IA updates DSAMS a management flag is produced notifying DFAS to close the lease case.

AP7.C4.18.5.5. Once the Lease is closed in Defense Integrated Financial System (DIFS), the IA opens the lease detail window "I" version, select "Update Implemented Lease" and update the Lease Condition Code in the Summary Tab. The normal condition code is TR (Termination and material Returned). Other selection options are TS (Termination and material scrapped), TP (Termination and an LOA is in process for Purchase), and TG (Termination and Grant in Process).

AP7.C4.18.5.6. The final step in Lease processing is for the IA to close the Lease. Select "subject-open-lease-milestone." Enter the Lease Designator and click “OK”. In the Lease Milestone List window, select "tools-MILDEP options-Close Lease." This posts the closure milestone to the lease and also updates the lease status (from Open to Closed).

The authority for granting of Excess Defense Articles (EDA) is contained in Section 505 of the Foreign Assistance Act (FAA). Please refer to the Appendix 8, Excess Defense Articles for detailed grant EDA program information. The management of EDA Grant cases is delegated to the appropriate IA. It is necessary for each Implementing Agency (IA) to ensure that Grant EDA cases under their cognizance are properly closed. Most IAs have the capability to certify zero value Grant EDA cases for closure using standard procedures. For those IAs whose management systems do not support the use of standard procedures, the following alternative closure process exists.

AP7.C4.19.1. Once the zero value Grant EDA case is ready for closure, the IA will load the (CLSEDAGRNT) milestone to the 'I' version of a Grant EDA case in Defense Security Assistance Management System (DSAMS), which will trigger a management flag (CLSEDAGRNTMF) to Defense Finance and Accounting Service - Indianapolis (DFAS-IN) informing them that the case is ready for closure.

AP7.C4.19.2. DFAS-IN will take action to close the Grant EDA case in Defense Integrated Financial System (DIFS) based on receipt of the management flag.

AP7.C4.20.1. Table AP7.C4.T7. lists the systems interfaces that occur prior to and during case closure.

Table AP7.C4.T7. Systems Interfaces

Click to view:

AP7.C4.21.1. Table AP7.C4.T8. reflects manpower funding guidelines pertaining to closure efforts:

Table AP7.C4.T8. Closure Manpower Funding

Closure Function | Funding Source |

|---|---|

Closure efforts for Supply/Services Complete (SSC) cases, to include non- Accelerated Case Closure Procedure (ACCP) and ACCP closures. | Foreign Military Sales (FMS) Administrative surcharge. |

Expedited case closure efforts requested by the purchaser beyond normal financial management standards. | A line on a new or existing case is preferred, although a line on a non-SSC case being reconciled could be used as well. |

AP7.C4.22.1. Table AP7.C4.T9. lists the primary Points of Contact (POCs) for active case reconciliation and closure issues.

Table AP7.C4.T9. General Point of Contact Matrix

Organization | Office |

|---|---|

Defense Security Cooperation Agency (DSCA) (Financial Policy & Regional Execution) | DSCA (Office of Business Operations, Financial Policy & Regional Execution Directorate (OBO/FPRE)) |

Army | United States Army Security Assistance Command (USASAC) New Cumberland (AMSAC-LAL-PCS) |

Navy | NAVY International Programs Office (IPO) (230C) |

Air Force | Air Force Life Cycle Management Center (AFLCMC)/WFCQ |

Defense Finance and Accounting Service - Indianapolis(DFAS-IN) | DFAS-IN/JAX |

Defense Contract Management Agency (DCMA) | DCMA-FB |