Active

There are no SAMM Changes as a result of this Policy Memo.

Contract Administrative Surcharge rates are updated in Chapter 9.

| DEFENSE SECURITY COOPERATION AGENCY | 6/3/2002 |

MEMORANDUM FOR :

DEPUTY UNDER SECRETARY OF THE ARMY

(DEFENSE EXPORTS AND COOPERATION)

(DASA(DE&C)/SAAL-ZN)

DEPARTMENT OF THE ARMY

DEPUTY ASSISTANT SECRETARY OF THE NAVY

(INTERNATIONAL PROGRAMS)

DEPARTMENT OF THE NAVY

DEPUTY UNDER SECRETARY OF THE AIR FORCE

(INTERNATIONAL AFFAIRS)

DEPARTMENT OF THE AIR FORCE

DIRECTOR, DEFENSE LOGISTICS AGENCY

DIRECTOR, NATIONAL IMAGERY AND MAPPING AGENCY

DIRECTOR, NATIONAL SECURITY AGENCY

DIRECTOR, DEFENSE CONTRACT MANAGEMENT AGENCY

DIRECTOR, DEFENSE CONTRACT AUDIT AGENCY

DIRECTOR, DEFENSE FINANCE AND ACCOUNTING SERVICE (DENVER CENTER)

SUBJECT :

FMS Contract Administrative Services (CAS) Surcharge Policy Improvements (DSCA 02-14)

As announced in the September 2001 Security Cooperation Conference, I chartered a team to review and recommend improvements to the FMS Surcharges. CAS was the first surcharge explored in depth. This memorandum announces the FMS financial policies and procedures for implementing the CAS improvements. Please note that some of the items discussed herein are effective immediately, while others will be implemented at a later time (e.g., FY2003).

The CAS improvements encompass clarifying its purpose and scope; establishing a revised rate structure, developing future rate validation guidelines; revising reciprocal agreement processes; and mapping the associated FMS case management transactions. For example, a major outcome regards the FMS CAS rate as shown below:

FMS CAS Component | For LOAs Implemented before 1 OCT 2002 | For LOAs Implemented On or After 1 OCT 2002 |

|---|---|---|

Contract administration/management | 0.50% | 0.65% |

Quality assurance & inspection | 0.50% | 0.65% |

Contract audit | 0.50% | 0.20% |

Outside CONUS (OCONUS) | Previously included above | 0.20% |

A summary of Attachments 1 through 5 that follow, which provide additional details on these improvements, is furnished on the page next under.

This package will be posted on the DSCA web site, Publications and Policy section (www.dsca.mil), and will be incorporated into the SAMM and DoDFMR, Volume 15.

In summary, I am confident that these policies represent real change and improvement to our FMS program. Its implementation and widespread practice will further promote business process efficiencies and increase customer satisfaction. To that end, I want to thank the individuals outside DSCA as noted in Attachment 6 for their outstanding contributions to this important endeavor. Please convey my personal appreciation for their dedication and professionalism, without which this endeavor would not have been accomplished.

Should your staff have any questions, the DSCA points of contact/Surcharge Team co-chairs are Mr. David Rude, telephone 703-604-6569, email david.rude@osd.pentagon.mil and Ms. Vanessa Glascoe, telephone 7036013744, email vanessa.glascoe@osd.pentagon.mil.

Tome H. Walters, Jr.

Lieutenant General, USAF

Director

ATTACHMENT :

As stated

CC :

Chairman Foreign Procurement Group Commandant, DISAM

OUSD (Comptroller)/ODCFO/F&MP

OUSD (AT&L/Foreign Contracting)

USASAC Alexandria

USASAC New Cumberland

NAVICP

AFSAC

SUMMARY OF ATTACHMENTS

Attachment 1: FMS CAS Purpose and Scope

One of the initial items the team addressed was to determine the purpose and scope of the FMS CAS surcharge. In that regard, Attachment 1 provides a matrix that correlates the FMS CAS functions with those specified in the Federal Acquisition Regulation (FAR). The matrix identifies those functions, categorizes them into the appropriate CAS pool, identifies the performing activity(ies), and provides additional comments as appropriate. We hope this matrix offers a better understanding of what CAS as regards FMS entails, and facilitates improved communications among the performing activities.

Attachment 2: FMS CAS Rate Assessment and Structure

The team reviewed the resource and funding efforts required to effectively execute the FMS CAS functions. Based on these findings, the means by which the CAS rate is assessed and the corresponding rate structure were revisited. The new CAS rate structure as described in Attachment 2 is effective with basic LOAs initiated in FY2003.

The long-term goal is to get to a process by which CAS is charged on an actual cost basis. This will be accomplished by DCMA and DCAA presenting to DSCA by 31 December 2002 a study for addressing the potential transition of FMS CAS to an actual cost basis on dedicated FMS CAS line(s) on an LOA. Based on this study, an assessment will be made to determine a course of action that is both beneficial, desirable and provides a clear return on investment.

Attachment 3: FMS CAS Surcharge Rate and Country Validation

The mechanics of this validation process, and the current tables relating to specific countries/international organizations, are described in Attachment 3.

Attachment 4: FMS CAS Reciprocal Agreements

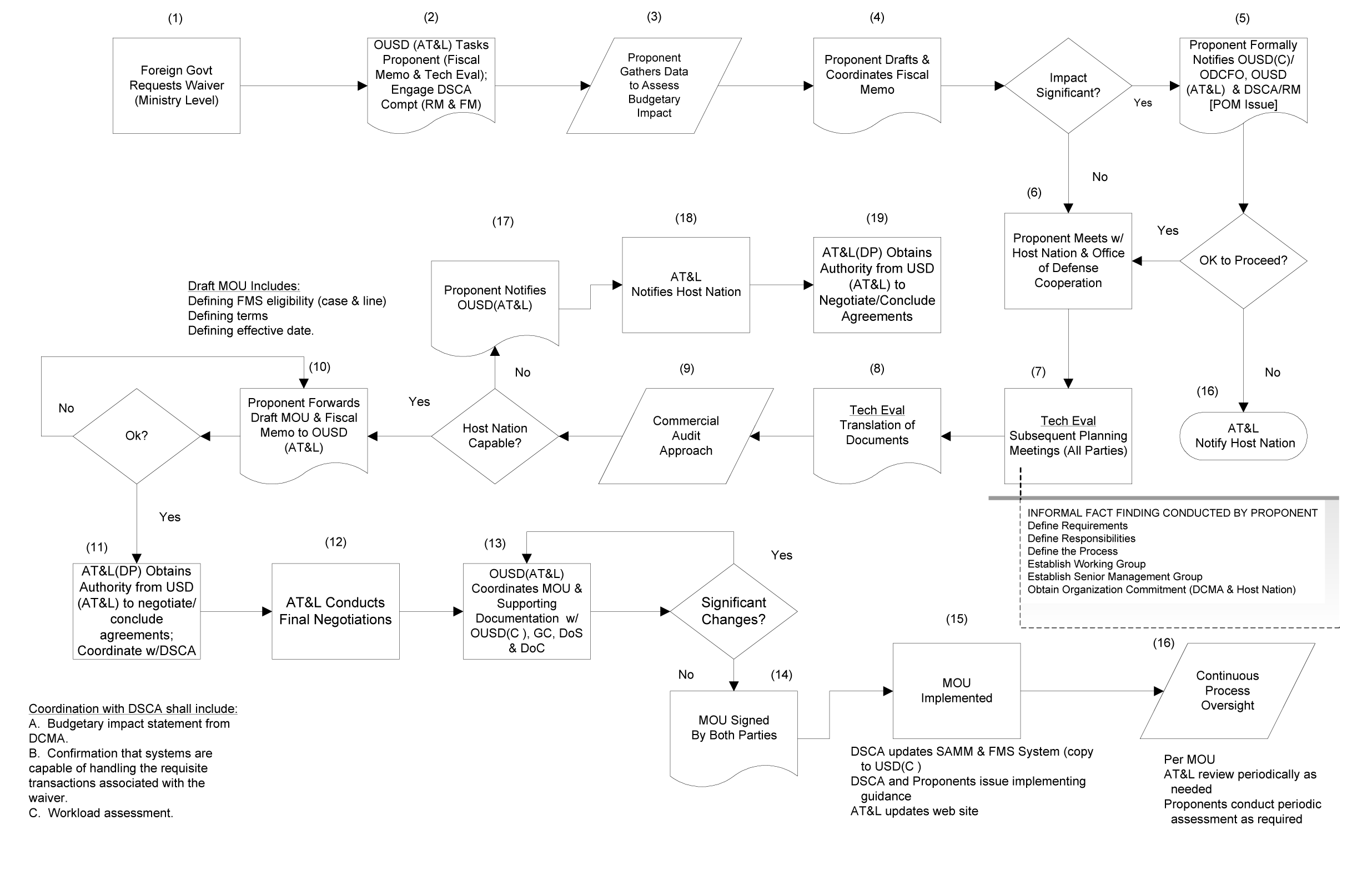

Attachment 4 is the flowchart depicting the FMS CAS-related reciprocal agreement process. In addition, under separate cover DSCA will forward to DoD General Counsel recommendations for improving DoD Directive 5530.3 (International Agreements), which assigns responsibility for controlling the negotiation and conclusion of agreements with foreign governments and international organizations by DoD personnel.

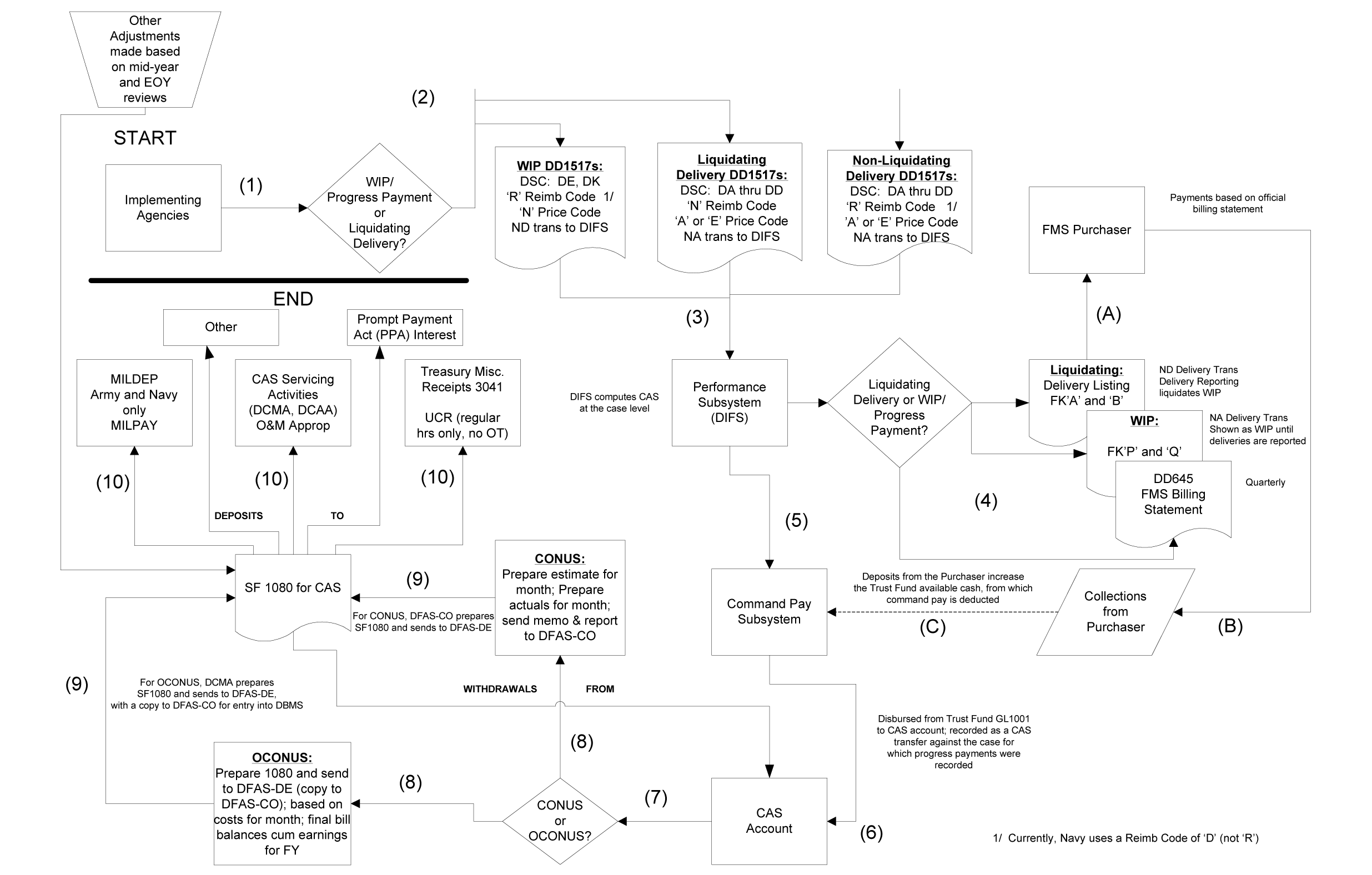

Attachment 5: FMS CAS Process Mapping

One of the key elements of managing FMS CAS is understanding the processes by which it operates. The team explored FMS CAS in the context of reciprocal agreements, budget formulation, LOA development and LOA execution. Separate flowcharts depicting these distinct yet related processes were developed, and are furnished at Attachment 5 (except for reciprocal agreements, noted in Attachment 4).

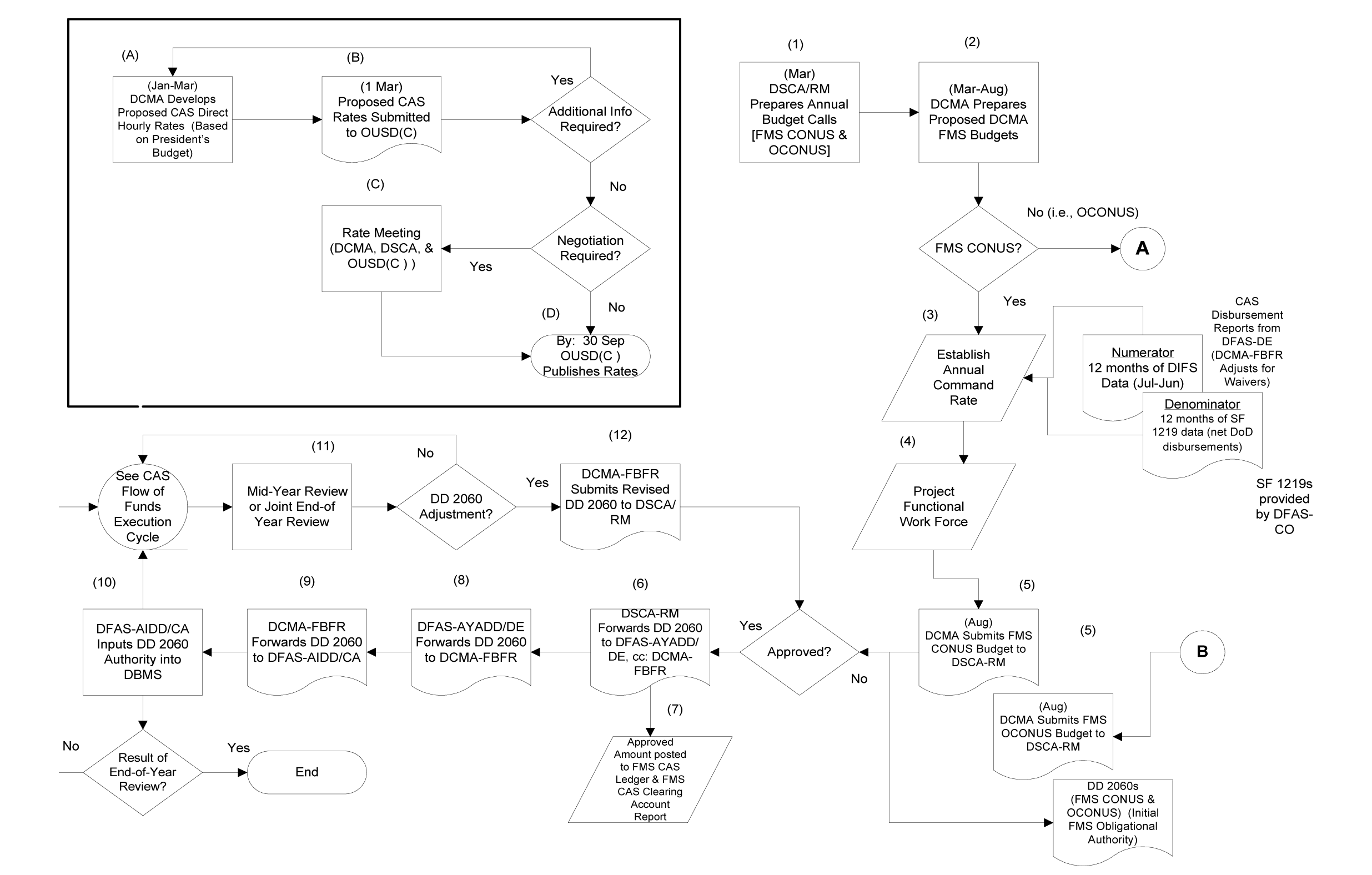

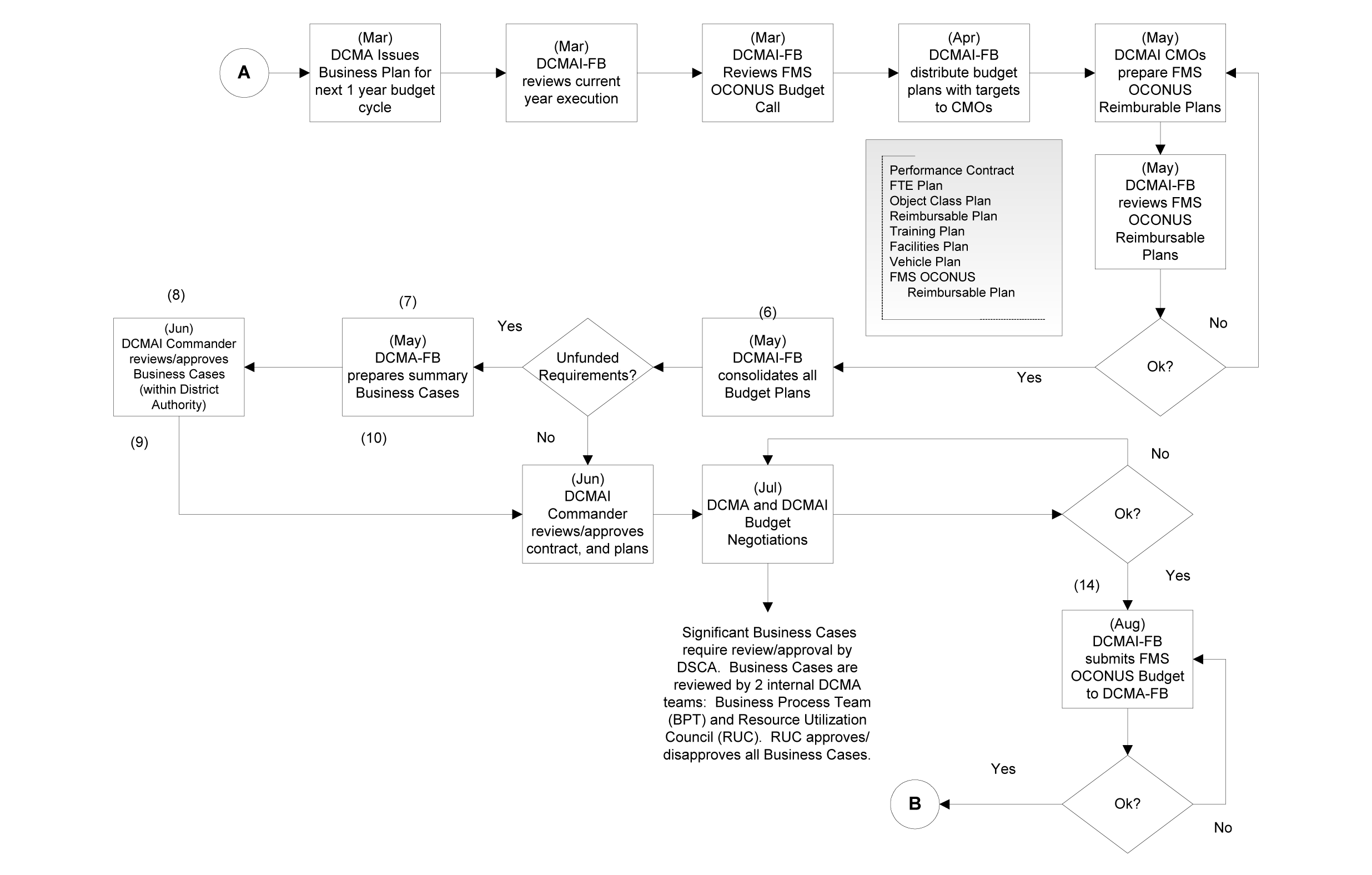

FMS CAS Budget Formulation. Refer to the flowchart provided at Attachment 5 (chart 5.1). To optimize the efficiency of the budget formulation process, DSCA/COMPT-RM will move the annual OCONUS budget call to the March timeframe, which is conducive to when DCMA International (DCMAI) issues the annual budget plan to its field activities.

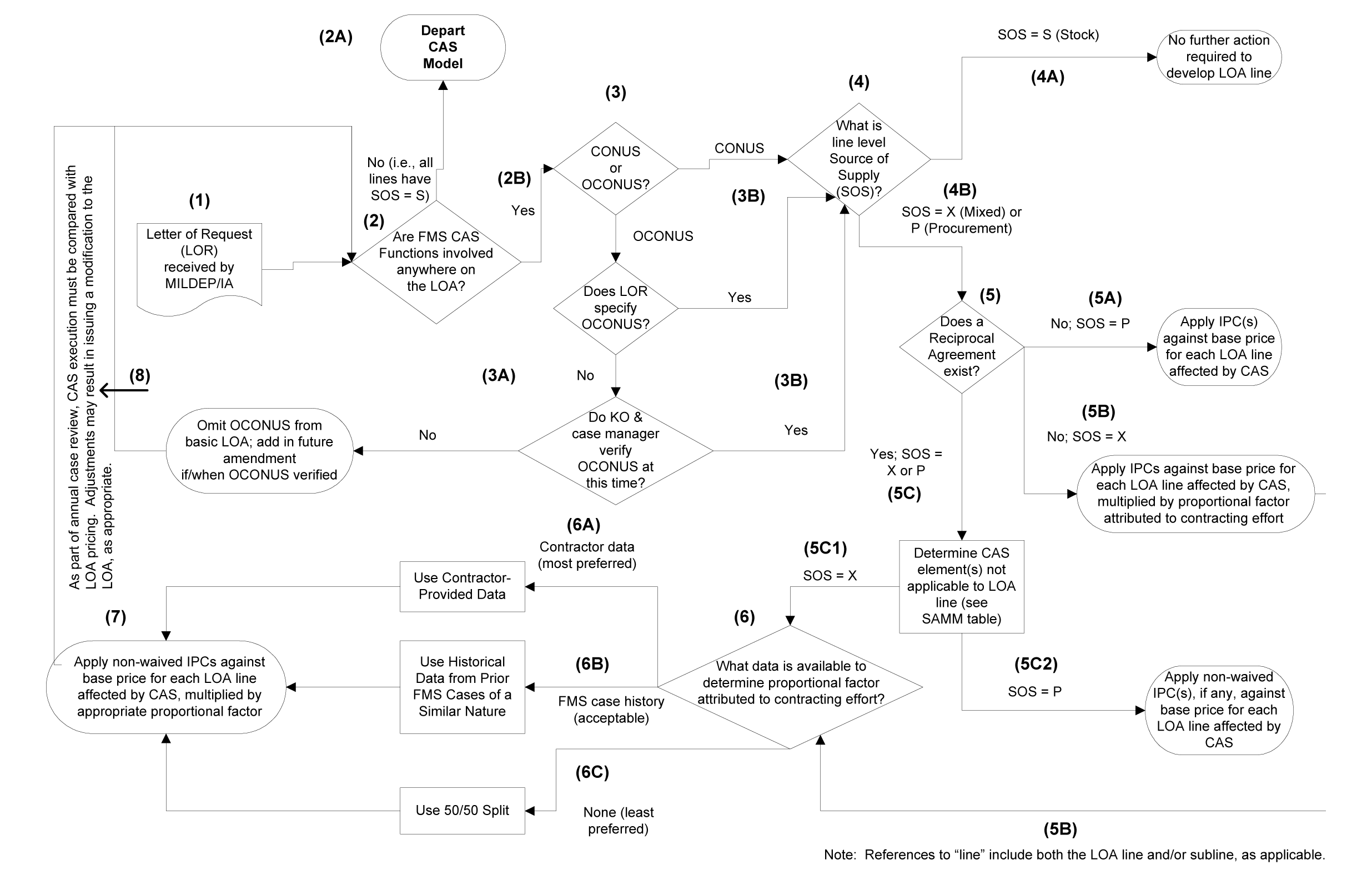

FMS CAS LOA Development. Refer to the business rules at Attachment 5, and the corresponding flowchart provided at Attachment 5 (chart 5.2).

FMS CAS Execution. Refer to the business rules at Attachment 5, and the corresponding flowchart provided at Attachment 5 (chart 5.3). That diagram is the foundation on which the detailed FMS CAS requirements for the Case Execution Management Information System (CEMIS) are being built.

FMS CAS Account Payment Components. Attachment 5 describes those efforts for which reimbursement from the FMS CAS Account is authorized.

Attachment 6: Surcharge Team.

Attachment 1 - FMS CONTRACT ADMINISTRATIVE SURCHARGE (CAS) FUNCTIONS

Federal Acquisition Regulation (FAR) Correlation Matrix

CAS Category | Performing Activity | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

FAR Function | FAR Function | Contract | QA & | Contract | DCMA | DCAA | MILDEPs | DFAS | DSCA | Comments |

42.101(a)(1) | Submit information and advice to the requesting activity, based on the auditor's analysis of the contractor's financial and accounting records or other related data as to the acceptability of the contractor's incurred and estimated costs. | x | x | |||||||

42.101(a)(2) | Review the financial and accounting aspects of the contractor's cost control systems. | x | x | |||||||

42.101(a)(3) | Perform other analyses and reviews that require access to the contractor's financial and accounting records supporting proposed and incurred costs. | x | x | |||||||

42.302(a)(3) | Conduct post-award orientation conferences (PAOCs). | x | x | x | x | MILDEPs (procuring contracting officer (PCO); DCMA (administrative contracting officer (ACO): receive/distribute/review contract; establish official contract file; analyze contract and assess risk; arrange PAOC; prepare Minutes/action items; identify support requirements; negotiate MOA/prepare support plan). | ||||

42.302(a)(4) | Review and evaluate contractors' proposals under Subpart 15.4 and, when negotiation will be accomplished by the contracting officer, furnish comments and recommendations to that officer. | x | x | x | DCMA: participate on IPT pricing team; reach agreement on overall team plan; discuss proposal with contractor; document objectives; negotiate with contractor to resolve remaining issues; prepare price negotiation memorandum; receive request for pricing assistance; receive approval of price negotiation; review/analyze contractor's proposal. MILDEPs: This is a primary function of the PCO. | |||||

42.302(a)(9) | Establish final indirect cost rates and billing rates for those contractors meeting the criteria for contracting officer determination in Subpart 42.7. | x | x | x | MILDEPs (submitting bills for final rates); DCAA (performing final overhead rate audits). | |||||

42.302(a)(12) | Review and approve or disapprove the contractor's requests for payments under the progress payments or performance-based payments clauses. | x | x | x | x | MILDEPs (PCO); DFAS (payments for proper invoices); DCMA (ACO). | ||||

42.302(a)(13) | Make payments on assigned contracts when prescribed in agency acquisition regulations. | x | x | |||||||

42.302(a)(14) | Manage special bank accounts. | x | x | |||||||

42.302(a)(15) | Ensure timely notification by the contractor of any anticipated overrun or underrun of the estimated cost under cost-reimbursement contracts. | x | x | |||||||

42.302(a)(17) | Analyze quarterly limitation on payments statements and recover overpayments from the contractor. | x | ||||||||

42.302(a)(24) | Negotiate and execute contractual documents settling cancellation charges under multi-year contracts. | x | x | |||||||

42.302(a)(27) | Approve contractor acquisition or fabrication of special test equipment under the clause at 52.245-18, Special Test Equipment. | x | x | x | ||||||

42.302(a)(30) | In facilities contracts: evaluate contractors requests for facilities; ensure required screening of facility items; approve use of facilities; ensure payment by contractor of any rental due; and ensure reporting of items no longer needed for USG production. | x | x | |||||||

42.302(a)(31) | Perform production support, surveillance, and status reporting, including timely reporting of potential and actual slippages in contract delivery schedules. | x | x | MILDEPs: PCO; DCMA: ACO. | ||||||

42.302(a)(38) | Ensure contractor compliance with contractual quality assurance requirements. | x | x | x | DCMA: review contract and identify customer requirements; perform risk assessment; develop risk handling plan and monitor risks; notify of actual/potential delays; document risk; monitor completion of production actions. MILDEPs: May involve a contracting officer's representative. | |||||

42.302(a)(40) | Perform engineering surveillance to assess compliance with contractor terms for schedule, cost, and technical performance in the areas of design, development and production. | x | x | |||||||

42.302(a)(41) | Evaluate for adequacy and perform surveillance of contractor engineering efforts and management systems that relate to design, development, production, engineering changes, subcontractors, tests, management of engineering resources, reliability and maintainability, data control systems, configuration management, and independent R&D. | x | x | DCMA: Review contract; provide input; identify key processes; identify required outcomes of processes and associated metrics; perform risk assessment; develop and implement risk handling plan; maintain risk documentation record. | ||||||

42.302(a)(42) | Review and evaluate for technical adequacy the contractor's logistics support, maintenance and modification programs. | x | x | |||||||

42.302(a)(43) | Report to the contracting office any inadequacies noted in specifications. | x | x | |||||||

42.302(a)(44) | Perform engineering analyses of contractor cost proposals. | x | x | |||||||

42.302(a)(45) | Review and analyze contractor-proposed engineering and design studies and submit comments and recommendations to the contracting office, as required. | x | x | |||||||

42.302(a)(46) | Review engineering change proposals for properclassification, and when required, for need, technical adequacy of design, productibility, and impact on quality, reliability, schedule and cost; submit comments to the contracting office. | x | x | |||||||

42.302(a)(49) | Monitor the contractor's value engineering program. | x | x | |||||||

42.302(a)(58) | Ensure timely submission of required reports. | x | x | x | MILDEPs: PCO; DCMA: ACO. | |||||

42.302(a)(64) | Negotiate and execute one-time supplemental agreements providing for the extension of contract delivery schedules up to 90 days on contracts with an assigned Criticality Designator of C (see 42.1105). Notification that the contract delivery schedule is being extended shall be provided to the contracting office. Subsequent extensions on any individual contract shall be authorized only upon concurrence of the contracting office. | x | x | |||||||

42.302(a)(65) | Accomplish administrative closeout procedures (see 4.804-5). | x | x | x | MILDEPs: PCO and FMS case manager, responsible for reconciling case records with underlying contracts; DCMA: ACO responsible for maintaining accurate contract administrative records (e.g., MOCAS); review contract closeout records; commence specialized closeout activities; administer final payment/closeout actions; prepare contract completion statement. | |||||

42.302(a)(67) | Support the program, product and project offices regarding program reviews, program status, program performance and actual or anticipated program problems. | x | x | x | x | MILDEPs: PCO; DCMA: Develop and execute program plan; prepare program status reports and charts; provide program integration; maintain program integration data. | ||||

42.302(a)(69) | Administer commercial financing provisions and monitor contractor security to ensure its continued adequacy to cover outstanding payments, when on-site review is required. | x | x | |||||||

42.302(a)(70) | Deobligate excess funds after final price determination. | x | x | x | MILDEPs: PCO; DCMA: ACO. Both are authorized to deobligate funds. | |||||

NOTES: | ||||||||||

Attachment 2 - REVISED FOREIGN MILITARY SALES (FMS)

Background

When compared to the revenue generated by the current 1.5% FMS CAS surcharge, the Surcharge team noted that the functions performed primarily by the Defense Contract Management Agency (DCMA) required funds exceeding the 1.0% allotted for quality assurance/inspection and contract administration. The contract audit effort performed predominantly by the Defense Contract Audit Agency (DCAA) costs less than the 0.5% allotted within the FMS CAS rate. The team also noted that $31M was infused into the FMS CAS account during the FY99/FY00 timeframe to ensure solvency. A major obstacle to the continued solvency of the FMS CAS account was the decision to charge the FMS Trust Fund, vice individual FMS cases for Outside the Continental United States (OCONUS) efforts effective 1 Oct 1993.

Based on these findings, the means by which the CAS rate is assessed and the corresponding rate structure were revisited. The new CAS rate structure as described below is effective with basic LOAs initiated in FY2003. Although the DCMA1 and DCAA systems that track CAS requirements provide some level of detail, neither system is currently capable of consistently identifying CAS at the individual FMS country/case/line level. Until those systems reach that level of sophistication, CAS will continue to be charged on a percentage (fixed rate) platform. This paper also describes the CAS rate assessment methodology, associated rates, DSAMS programming requirements, and implementation timeline.

By 30 June 2002, OUSD (Comptroller) will issue an interim change to the Department of Defense Financial Management Regulation (DoD FMR), Volume 15, authorizing the CAS rate changes.

Revised Rate and Rate Structure

Effective with new (basic) Letters of Offer and Acceptance (LOAs) implemented on or after 1 October 2002, the rate and rate structure for FMS CAS changes. For LOAs implemented prior to 1 October 2002, the previous FMS CAS rates apply for the remaining life of those LOAs. In addition, Outside the Continental United States (OCONUS) efforts shall now be charged separately from the other categories relating to FMS CAS: quality assurance and inspection; contract audit; and contract administration. The following table applies:

FMS CAS Component | For LOAs Implemented | For LOA Implemented On |

|---|---|---|

Contract administration/mgmt | 0.50% | 0.65% |

Quality assurance & inspection | 0.50% | 0.65% |

Contract audit | 0.50% | 0.20% |

Subtotal, CONUS FMS CAS | 1.50% | 1.50% |

Outside CONUS (OCONUS) | Previously included above | 0.20% |

Total, CONUS + OCONUS FMS CAS | 1.50% | 1.70% |

See "Defense Security Assistance Management System (DSAMS) Changes" section below for information about developing LOA documents in DSAMS that incorporate these revisions.

OCONUS Impact

The separation of OCONUS as an additional FMS CAS component requires a clear channel of communication between the contracting officer, DCMA and the FMS case manager. It involves a two-pronged approach: OCONUS request and OCONUS confirmation. Optimally, the purchaser's desire for OCONUS CAS should be stated in the Letter of Request (LOR) whenever possible. In less than optimal conditions, if the OCONUS CAS effort is identified after basic LOA implementation, that would constitute a change in scope - thus, an amendment to the LOA would be required. The new CAS rate, to include the OCONUS component, would apply as of the basic LOA implementation date. If necessary, DFAS will manually adjust the CAS accruals for any applicable progress payments occurring prior to amendment issuance. An amendment may immediately follow basic LOA implementation, which is less desirable than the OCONUS designation in the LOR, but is preferred to waiting until the execution phase already commenced. In any event, the procuring contracting officer (PCO) must confirm the existence of OCONUS to the performing activity and especially the FMS case manager. This process will be aided by ensuring that the FMS case identifier is clearly displayed in the contract line item number (CLIN). DSCA will explore whether the Defense Federal Acquisition Regulation Supplement (DFARS) should be revised to stress these relationships.

The OCONUS component requires special focus on the contracts being administered outside of CONUS. This influences specific cost drivers, particularly labor, personal services, personnel change of station (PCS) and facilities. Accordingly, the costs necessary to capture the OCONUS effort must reflect these intensified efforts.

Revised Rate Structure Methodology

Defense Security Assistance Management System (DSAMS) Changes

- By 31 May 2002, the DSAMS shall incorporate a new Indirect Price Component (IPC) for OCONUS; this would result in a total of four CAS-related IPCs potentially applicable to a given LOA..

- A standard note would be placed in the LOA that notifies the FMS purchaser as to the total CAS estimated. The CAS note shall include the rate, each CAS component that applies, and each CAS component that does not apply (i.e., a waiver impacts the CAS for that LOA). Different sets of notes will be used for pre-FY03 and post-FY02 LOAs (based on basic LOA implementation date).

By 31 May 2002, two standard "boilerplate" notes will be programmed into DSAMS by each MILDEP as follows:

Standard Note 1: For any lines on this LOA document with a Source of Supply of 'X' or 'P', the Contract Administrative Surcharge (CAS) rates apply: for contract administration; ___%; for quality assurance and inspection, ___%; and for contract audit, ___%. Standard Note 2: For any lines on this LOA document with a Source of Supply of 'X' or 'P', the Contract Administrative Surcharge (CAS) rates apply: for contract administration; ___%; for quality assurance and inspection, ___%; for contract audit, ___%; and for overseas CONUS, ___%. If a CAS waiver does apply, either note should be expanded to include the following statement: "A waiver is authorized for the following CAS components: (fill in those that apply)." . For basic LOAs prepared before 1 Oct 2002 with an Offer Expiration Date (OED) on or after 1 Oct 2002, case writers are to use the Override Percent (OP) feature and load the revised rates as shown above. For basic LOAs prepared after 1 Oct 2002, case writers are to use the new CAS rates that will be loaded into DSAMS by 31 May 2002. For LOA amendments that introduce new lines on an LOA, which are prepared after 1 Oct 2002 for basic LOAs implemented prior to 1 Oct 2002, case writers are to use the OP feature and load the pre-FY03 rates shown above. This requirement will be necessary until DSAMS is reprogrammed to capture all CAS rate scenarios automatically. |

Illustration of CAS Pricing Computation

Given current DIFS constraints, the total CAS surcharge would be assessed at the case level until DIFS can accommodate line-level CAS computations. An illustration follows:

Given: | Case BN-Q-ABC |

Basic LOA Implementation Date: | 15 October 2002 |

Total LOA Articles/Services Value: | $100,000 |

Source of Supply = | 'P' (Procurement) for all lines |

| |

CAS Pricing: |

|

QA and Inspection | $ 650.00 |

Contract Audit | 200.00 |

Contract Admin | 650.00 |

Overseas CONUS | 200.00 |

Total CAS Applied | $1,700.00 |

DFAS will load into DIFS a 1.7% CAS surcharge for the case. The 1.7% CAS would be assessed against the progress payments reported, as is done today. If OCONUS does not apply, that IPC is not factored into the CAS pricing for that LOA (and, in the preceding example, a 1.5% CAS surcharge would apply).

Benefits to FMS Purchasers:

- Annual rate and rate structure validation allows for more flexible CAS reimbursement to CAS performing activities and CAS billing for customers to reflect values closer to actual costs.

- Revised rate structure implements necessary realignment of percentages for CAS-related components, including OCONUS.

- Allows for periodic validation of the CAS percentages applicable to each of the four FMS CAS categories/IPCs.

- Provides improved detail to the FMS purchaser.

- Precedence exists (i.e., FMS administrative) for varying percentage-based rates applicable to a specific FMS surcharge.

- Allows for eventual migration to (a) CAS assessed at the line level (with no change to the methodology described above), and/or to (b) actual cost basis.

NOTE: 1 The methodology for calculating FMS CONUS CAS earnings for DCMA is outlined in the 9 Apr 1999 CAS Memorandum of Agreement between DCMA, the Defense Finance and Accounting Service (DFAS) and DSCA. FMS OCONUS CAS earnings are calculated on an actual cost basis at the country level.

Attachment 3 - CAS RATE AND COUNTRY VALIDATION

Rate Validation

The FMS CAS surcharge rate shall be validated annually by DSCA Comptroller, and submitted to OUSD (Comptroller, DCFO, Finance and Management Policy) for approval. The annual validation will occur by 31 December of each year, and will include a review of the prior fiscal year's FMS CAS-related collections and expenditures (the latter by performing activity). The primary performing activities (DCMA and DCAA) will continue to provide documentation evidencing improved management efficiencies. For example, DCAA will continue to provide this information as part of the budget estimate/hourly reimbursable rate process previously established by DoD Comptroller. Alternatively, performing activities may document these improvements in response to DSCA's annual budget calls and development of the FMS CAS rate. Lastly, the annual DSCA Comptroller validation will include verifying the inventory of countries and international organizations for which a waiver of the FMS CAS applies either in whole or in part. DSCA Comptroller will include the performing activity's input into its rate validation assessment, solicit coordination from those activities on that assessment, and submit the package to OUSD (Comptroller/ODCFO/F&MP) for approval. This document identifies the current tables relating to the affected countries/international organizations. These updated tables will be reflected in the next Security Assistance Management Manual (SAMM, DoD 5105.38-M) revision.

Country/International Organization Rates

When CAS work is performed on FMS cases that have CAS waivers, the cost of the CAS efforts (contract audit; quality assurance and inspection; and contract administration services) shall be funded by any DoD appropriation having sufficient funds to absorb the cost of those efforts waived. Billings for actual costs shall not be submitted for reimbursement against the FMS CAS Surcharge Account. Countries, NATO projects or organizations and other CAS waiver agreements are illustrated in the following three tables. Additions, changes or deletions to the tables will be updated by the DSCAComptroller/ FM after coordination with the DoD proponent organization.

Table 1 reflects a listing of approved reciprocal country agreements. The waiver under each reciprocal agreement applies only to new FMS LOAs with implementation dates, on or after the Effective Date of the reciprocal agreement and as recorded in DIFS (Does not apply to individual LOA lines, contracts or amendments to LOAs). All systems should contain the same date as the reciprocal agreement and DIFS records.

Table 1 - APPROVED RECIPROCAL COUNTRY AGREEMENTS

Country | Effective Date | Cost Waived |

|---|---|---|

Belgium (BE) | 26 Apr 1983 | Quality Assurance and Inspection |

Canada (CN) | 27 Jul 1956 1 Apr 1984 | Contract Audit Quality Assurance and Inspection |

Denmark (DE) | 3 Apr 1985 | Quality Assurance and Inspection |

France (FR) | 17 Jul 1981 23 Apr 1986 | Contract Audit Quality Assurance and Inspection Contract Administration Services |

Germany (GY) | 6 Dec 1983 | Quality Assurance and Inspection Contract Audit |

Greece (GR) | 23 Sep 1992 | Quality Assurance and Inspection |

Italy (IT) | 7 Jan 1983 | Quality Assurance and Inspection |

Netherlands (NE) | 9 Apr 1982 | Quality Assurance and Inspection Contract Audit |

Norway (NO) | 23 Nov 1986 | Quality Assurance and Inspection |

Spain (SP) | 12 Jun 2000 | Quality Assurance and Inspection |

Turkey (TK) | 12 Mar 2001 | Quality Assurance and Inspection |

United Kingdom (UK) | 30 Oct 1979 | Contract Audit Quality Assurance and Inspection |

The National Institute of Standards and Technology Codes : CA=Canada, DA=Denmark, GM=Germany and NL= Netherlands | ||

Table 2 - APPROVED AGREEMENTS/WAIVERS RELATIVE TO PARTICIPATING GROUPS/ ORGANIZATIONS/PROJECTS.

Groups/ Organizations/ Projects | Effective Date | Cost Waived |

|---|---|---|

European Participating Governments (EPG): | 19 December 1980 | Contract Audit Quality Assurance and Inspection |

Mid-Life Update Production Phase Cases and new F-16 LOAs implemented on or after effective date. | 5 April 1993 | Contract Audit |

The remainder of the F-16 LOAs for BE, DE, NE, & NO will get the CAS waivers that are reflected in the Country Code Table 1. |

|

|

United Kingdom Polaris Project (UZ) | OUSDC memo 27 Oct 1995 | Contract Audit |

Table 3 - APPROVED NATO AGREEMENTS

This table will be furnished separately, once the FMS community determines the consensus architecture of the NATO Infrastructure programs.

Attachment 4 - CONTRACT ADMINISTRATIVE SERVICES (CAS)

RECIPROCAL BILATERAL DEFENSE PROCUREMENT

REVISED PROCESS - APRIL 2002

Attachment 5 - FMS CAS BUSINESS RULES

FMS CAS LOA Development

The following LOA development business rules are emphasized:

- Whenever possible, the purchaser's desire to include OCONUS as part of an LOA should be specified in the Letter of Request (LOR).

- Efficient channels of communication amongst the procuring contracting officer, FMS case manager, and CAS performing activities (e.g., DCMA, DCAA) must exist, in part to verify in a timely manner the requirement for OCONUS CAS. This relationship is also critical to confirm the extent to which FMS CAS actually applies on LOA lines/sublines coded with a Source of Supply (SOS) of 'X' (mixed stock/procurement). Chart 5.2 delineates the preferences for ascertaining the extent to which contractual actions apply to a given LOA line.

- CAS is not priced on the LOA if all LOA lines/sublines are coded with a SOS of 'S' (for stock).

- Care must be taken to appropriately assess (or not assess) CAS for each Indirect Pricing Component (IPC).

A new standard LOA note is required on all LOA documents, effective 1 Oct 2002. Refer to Attachment 2 for additional information.

FMS CAS Execution

The following business rules are stressed:

- FMS CAS will continue to be assessed against progress payments and final deliveries - irrespective of the SOS assigned to a given LOA line.

- The progress payment and delivery transactions involve specific and unique delivery source codes, reimbursable codes, price codes and transaction types for the MILDEPs and DFAS. Care must be taken to ensure an accurate accounting of FMS CAS computations. Refer to Chart 5.3.

- The annual case review checklists developed by the MILDEPs/Implementing Agencies (IAs), which are based on DSCA policy memo 01-22 dated 19 September 2001, shall include a requirement to validate CAS pricing accuracy. This entails ensuring a linkage exists between actual CAS-related execution performance with the current CAS pricing profile as contained in DSAMS. The annual review may necessitate adjustments to the DSAMS CAS pricing structure and issuance of a corresponding LOA modification.

To the extent OCONUS is identified on or after the 1 October 2002 basic LOA implementation date, the MILDEP/IA shall be responsible for modifying the LOA. This entails (a) specifying the revised CAS rates in the LOA note and (b) case managers notifying their DFAS Denver counterparts in order for DFAS to manually adjust CAS accruals for any applicable progress payments reported prior to the inclusion of the OCONUS rate.

FMS CAS Account Payment Components

The following describes those efforts for which reimbursement from the FMS CAS account is authorized:

- Earnings to DCMA, DCAA and other CAS-performing activities for FMS CAS work.

- Military Pay to MILDEPs as regards FMS CAS duties performed by USG military personnel.

- Unfunded Civilian Retirement (UCR) is paid to the U.S. Treasury Miscellaneous Receipts account 3041 as regards UCR associated with USG civilian personnel performing FMS CAS duties.

Any transaction not in direct support of FMS CAS efforts shall not be paid from the FMS CAS account.

CONTRACT ADMINISTRATION SERVICES (CAS)

BUDGET FORMULATION CYCLE (Page 1 of 2)

REVISED PROCESS APRIL 2002

CONTRACT ADMINISTRATION SERVICES (CAS)

BUDGET FORMULATION CYCLE (Page 2 of 2)

REVISED PROCESS APRIL 2002

CONTRACT ADMINISTRATIVE SERVICES (CAS)

LOA DEVELOPMENT CYCLE

REVISED PROCESS APRIL 2002

CONTRACT ADMINISTRATIVE SERVICES (CAS)

FLOW OF FUNDS : EXECUTION CYCLE

REVISED PROCESS APRIL 2002

Attachment 6 - SURCHARGE TEAM: FMS CAS PARTICIPANTS (USG OFFICIALS)

ARMY

- Sherry Ownby, DASA(DE&C)

- Reginald Graham, USASAC

- Barbara Dowdy, USASAC St. Louis

NAVY

- Chris Chaikowski, IPO

- Donald Temple, NAVICP

- Morris Zupan, NAVICP

- Jane Downer, NAVAIR

- Karen Adler, NAVAIR

AIR FORCE

- Colleen Henson, SAF-IAPX

- Sheilah Boyd, SAF-IAPX

- Charles Pope, SAF-FMBIS

DFAS

- Tom McIntire, DFAS-DAC

- Dixon Weaver, DFAS-AY/DE

DCMA

- Val Brown, FBFR

- Deana Lande, FBFR

- Melanie Ammann, DCMAI

- Berthina Jamison, DCMAI

- Bob Hunter, DCMAPI

- James Davenport, FBFR

DCAA

- Linda Ebersbach

- Cris Hornsleth

- Judy Maness

- Bill Torrick

- Joe Garcia

OUSD (Comptroller)

- Tom Hafer

- Becky Allen

- OUSD (AT&L)

- Mike Mutty

DSCA

- David Rude, COMPT-FM

- Vanessa Glascoe, COMPT-FM

- Paul Kopicki, COMPT-RM

- Greg Sutton, DISAM

- John Clelan, DISAM

- Steve Harris, P3-P2

- Cindy Leach, COMPT-FM

- Chester Freedenthal, IT

- LtCol Ron Todd, USAF, OGC

- Joy Marcou, COMPT-FM